From Feature Creep to Subscription Fatigue

Fitness wearables have spent more than a decade accumulating features, until fitness trackers, smartwatches, and running watches blurred into a single device category overloaded with capabilities many buyers never use. As the market reached saturation and upgrades delivered diminishing real-world benefits, hardware makers looked elsewhere for growth. Subscriptions became the obvious answer: instead of relying on people to replace a watch every few years, companies could charge recurring fees for advanced analytics, coaching, and cloud-based insights. Whoop leaned hardest into this model, offering a minimalist strap while positioning its app and continuous data analysis as the true product in a fitness tracker subscription. But as consumers grew more comfortable with wearable health tracking, the value of paying every year for what felt like incremental software improvements started to come under pressure, especially once cheaper hardware caught up on core health metrics.

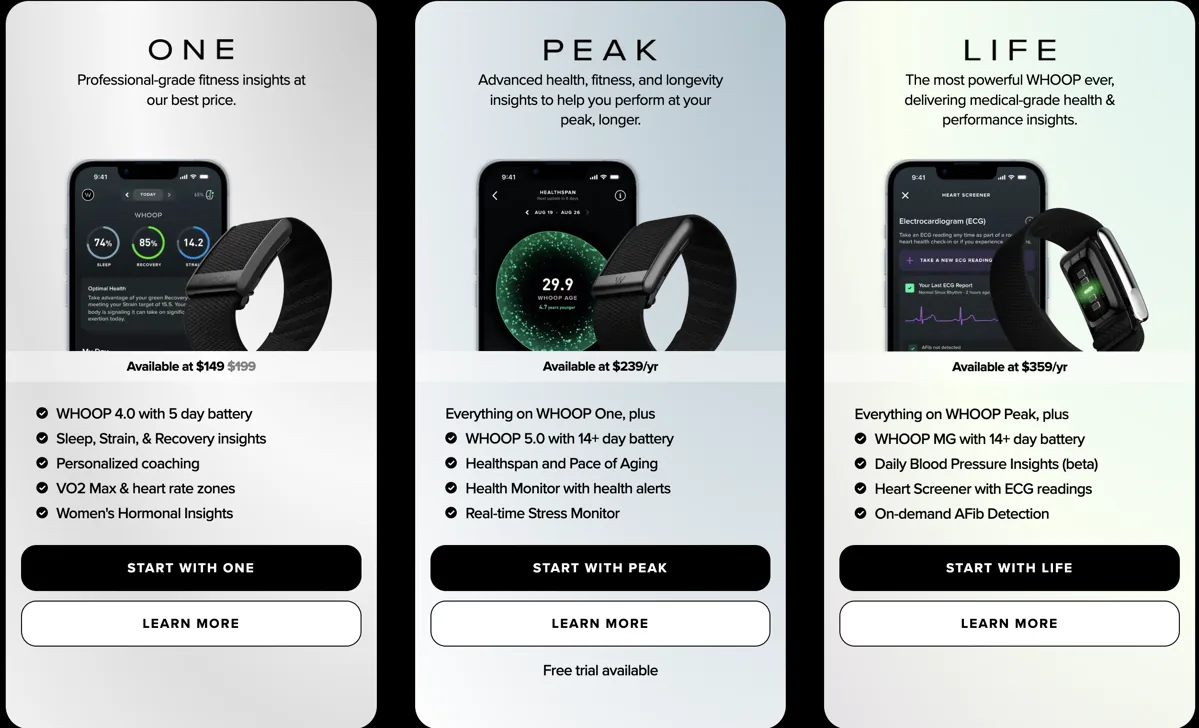

Whoop’s Subscription Model Meets Real Competition

For years, Whoop enjoyed a near monopoly in smart bands: a simple strap, clever charging system, and an app rich in recovery, sleep, and training insights. The hardware itself was intentionally basic, while the business hinged on a recurring fee that could reach hundreds of dollars annually, positioning Whoop as a service rather than a gadget. That proposition resonated with serious athletes willing to pay for detailed guidance. However, demand also existed among everyday users who wanted similar metrics without a long-term fitness tracker subscription. Forum threads frequently asked about Whoop alternatives but had few credible options. That landscape is now shifting. New bands from established brands have entered the market, narrowing the gap in data collection and analysis. As similar hardware becomes widely available, Whoop’s premium pricing must increasingly be justified by unique metrics, coaching quality, and a broader health-services ecosystem rather than by hardware exclusivity alone.

Affordable Fitness Trackers Redraw the Value Line

The arrival of basic smart bands like Polar Loop, Amazfit Helio Strap, and Garmin’s Index sleep band signaled a reset in wearable design priorities. Instead of chasing ever larger screens and app-like experiences on the wrist, these devices strip things back to sensors and straps, leaving the heavy lifting to smartphone apps. That simplicity also helps lower prices, making affordable fitness trackers newly appealing to users who primarily care about accurate heart rate, sleep, and activity data. The real inflection point is Google’s Fitbit Air, a smart band priced at USD 99 (approx. RM460) that promises analytics and coaching comparable to Whoop’s, but without recurring fees. If its health app delivers even “good enough” insights, many consumers will perceive a one-time purchase as far better value than a USD 239 (approx. RM1,110) yearly subscription, especially for casual athletes and wellness-focused users rather than performance-obsessed competitors.

Shifting Consumer Expectations in Wearable Health Tracking

As more Whoop alternatives emerge, the baseline expectation for wearable health tracking is changing. Consumers increasingly assume that continuous heart rate monitoring, sleep staging, and basic recovery indicators should come included with the device, not paywalled behind a subscription. Subscriptions now have to justify themselves with genuinely differentiated offerings—human coaching, medical-grade integrations, or advanced metrics that meaningfully change behavior. Whoop is already repositioning toward a broader health-services identity, adding options like blood tests and paid video consults, signaling that it sees its future beyond a simple band-and-app bundle. Meanwhile, competitors evolve their apps, turning affordable fitness trackers into platforms rather than accessories. This divergence suggests a market where casual users gravitate toward one-time purchases with robust apps, while a smaller niche pays for premium, service-heavy subscriptions tied to performance, rehabilitation, or clinical use cases.

Fragmentation, Choice, and the Future of Fitness Tracker Subscriptions

The smart band category’s reboot is fragmenting the market in a way that ultimately benefits buyers. On one end sit minimalist bands like Fitbit Air and Amazfit’s strap-style devices, catering to price-sensitive users who want straightforward data and light coaching without recurring charges. On the other end remain high-touch services like Whoop, which still appeal to athletes and data enthusiasts who value advanced recovery tracking and emerging health offerings enough to pay ongoing fees. In between, brands like Garmin and Polar experiment with hardware-light devices that plug into existing app ecosystems. This layered landscape reduces the pressure for a one-size-fits-all solution and undermines the notion that serious health insights must come with an expensive fitness tracker subscription. Instead, subscriptions are becoming optional add-ons atop increasingly capable, affordable hardware—a shift that could force all players to innovate on service quality rather than lock-in.