Finance Automation M&A: From Fragmented Tools to CFO Platforms

Finance automation M&A is the trend where software, banking, and investment firms buy and combine accounts payable, receivable, planning, tax, and procurement tools into larger, AI‑enabled financial operations platforms that give CFOs broader workflow coverage, deeper automation, and tighter control over data and decisions. Coupa’s acquisition of Rossum is a clear signal: intelligent document processing has moved from a handy add‑on to a core capability for enterprise finance automation. By fusing Rossum’s large language model and OCR invoice capture with payments, cash management, AP workflows, and spend visibility, Coupa is turning AP into a smarter, data‑rich command center. Across AP, AR, FP&A, financial close, e‑invoicing, and spend management, similar deals are pulling the market away from point solutions and toward integrated platforms built for the office of the CFO, with integration and AI as the main value drivers.

Who Is Buying What: The New Finance Automation Power Map

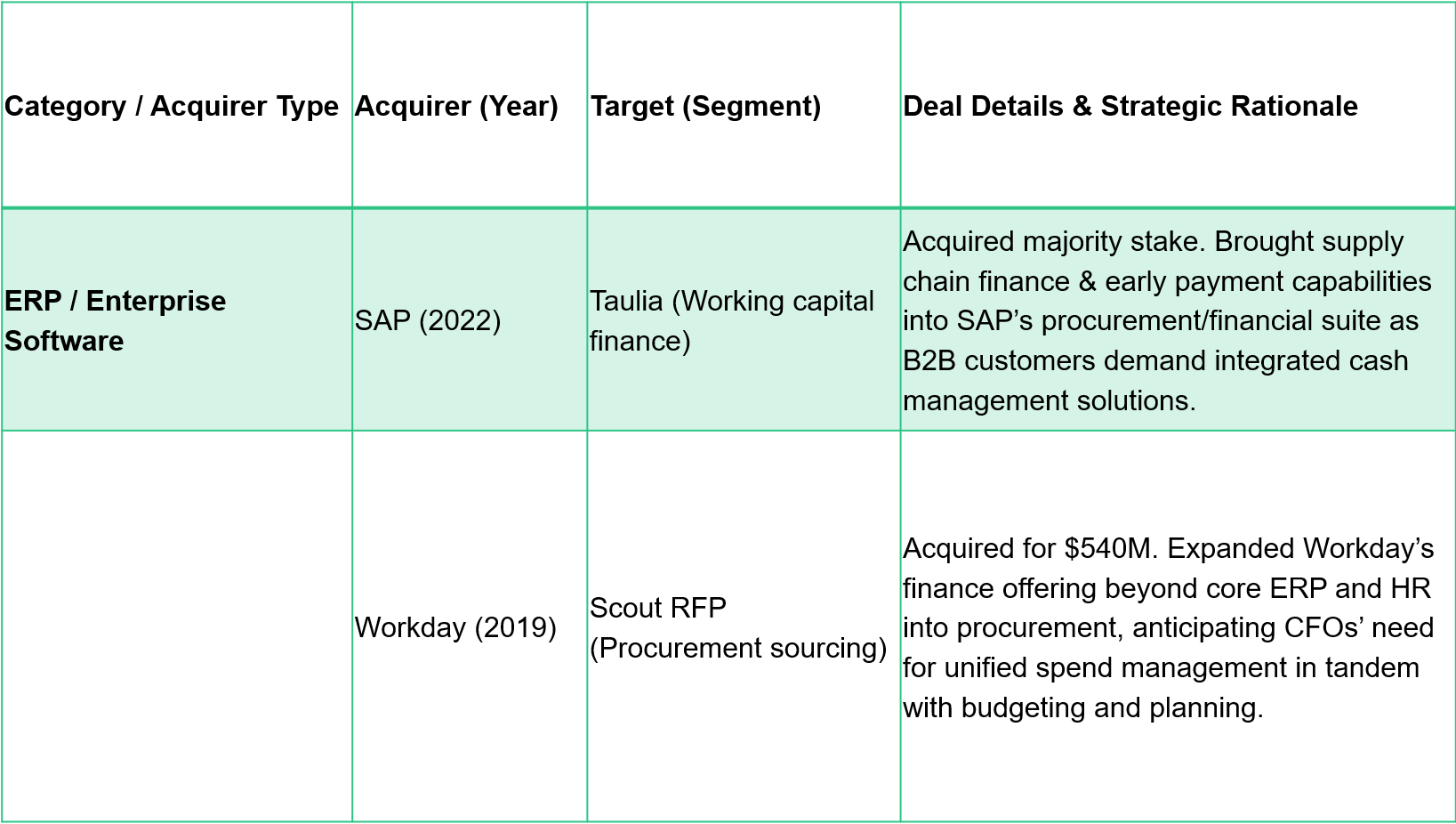

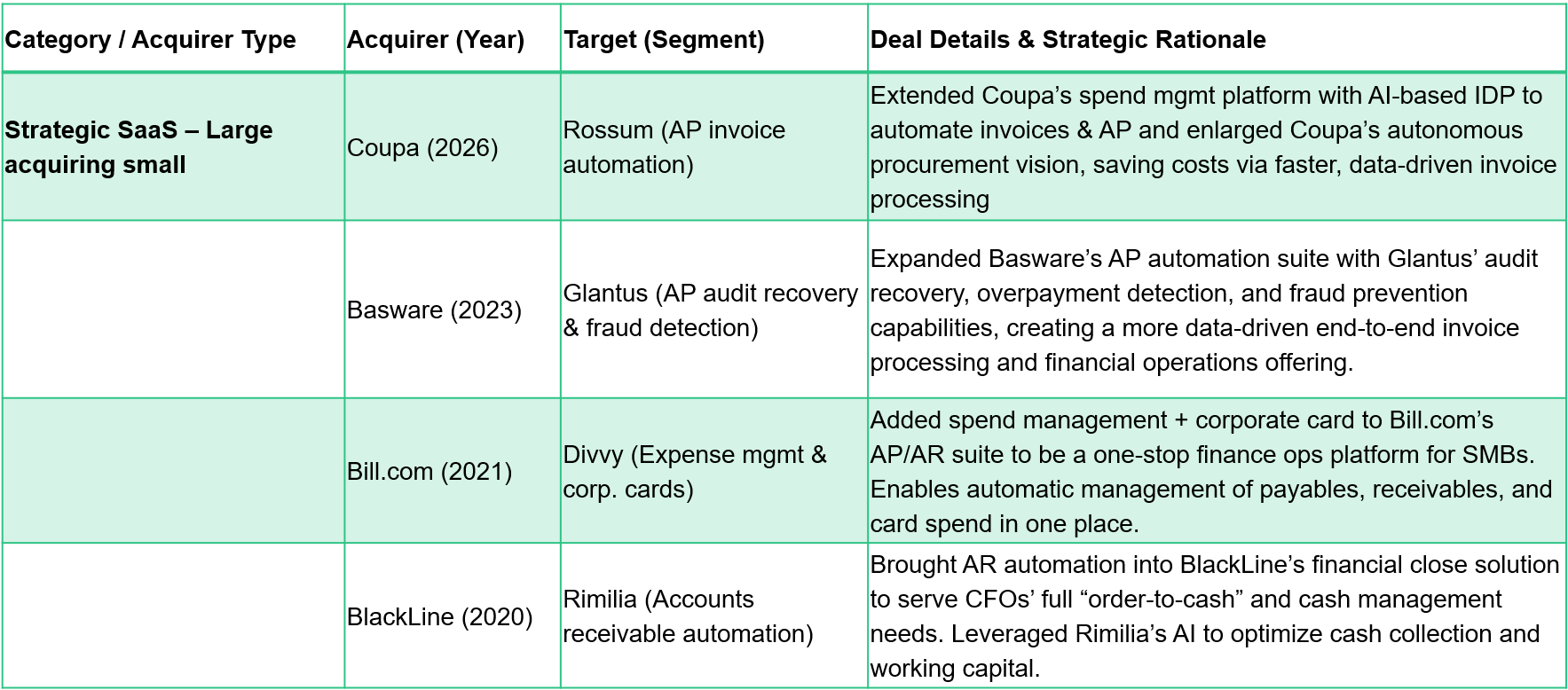

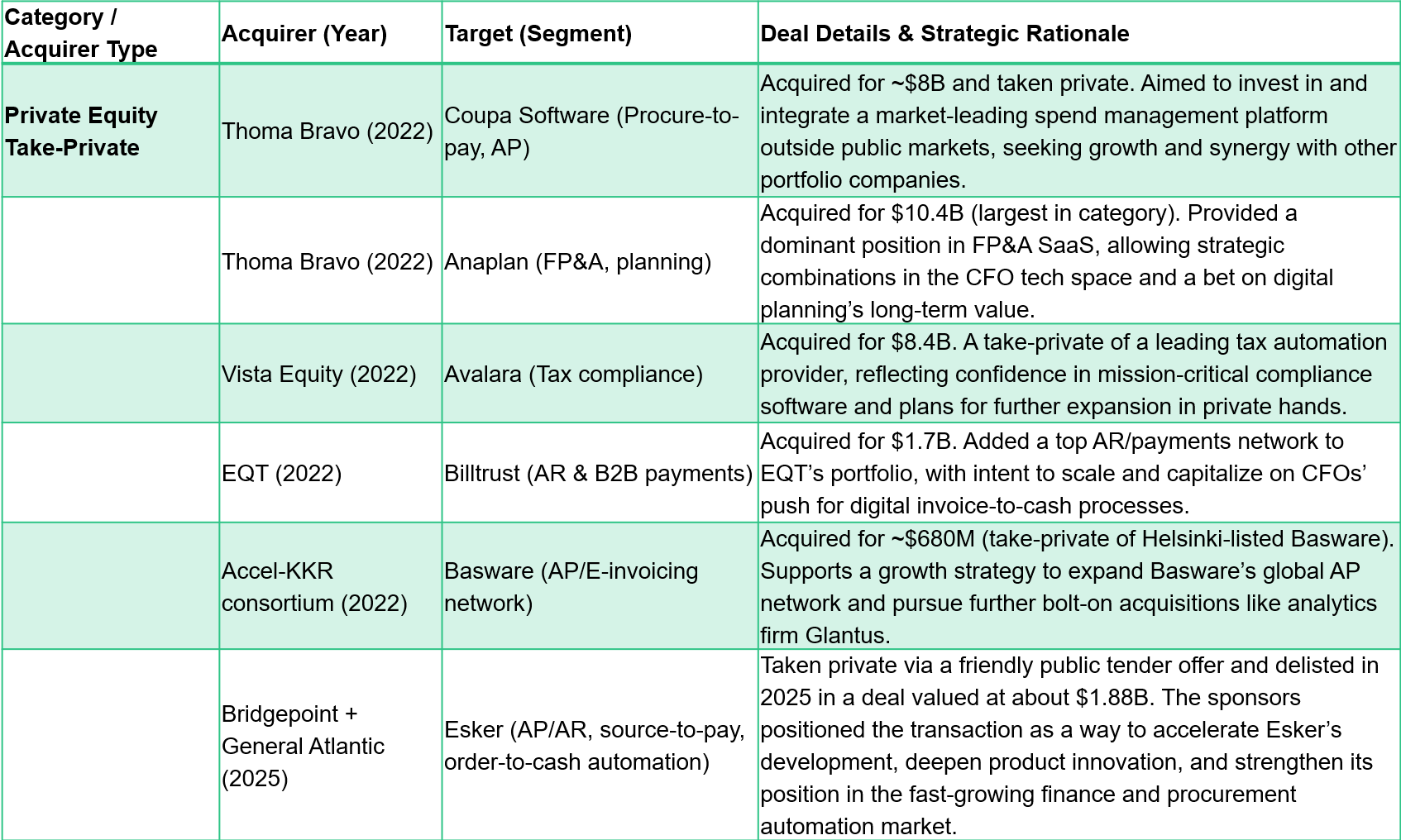

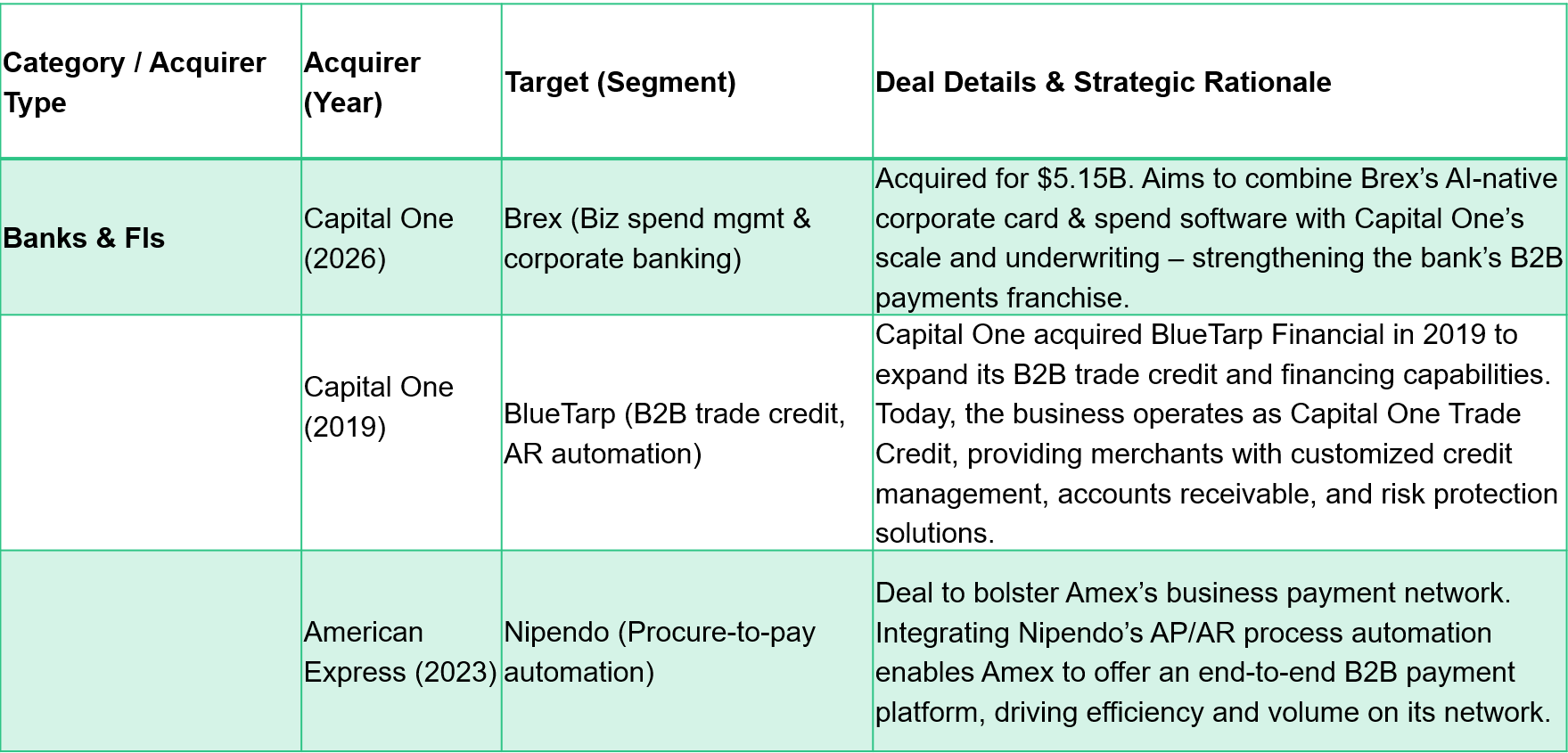

The current wave of finance automation M&A is powered by four distinct buyer groups, each reshaping enterprise software consolidation in its own way. Strategic SaaS vendors are snapping up specialist AP, AR, and spend tools to deepen workflows, as seen in Bill.com buying Divvy, BlackLine acquiring Rimilia, and Coupa adding Rossum. Private equity firms have taken platforms such as Anaplan, Avalara, Basware, Billtrust, Coupa, and Esker private to build durable CFO platforms with room for bolt‑on deals and margin expansion. Banks and card networks are moving up the stack, with Capital One and American Express acquiring automation platforms to own workflows, not only payment rails. ERP providers like SAP and Workday are selectively filling finance automation gaps, adding working capital, planning, and procurement without forcing full suite replacement, then focusing on cloud integration and embedded AI instead of more aggressive acquisitions.

AI-Native Decision Engines: The Missing Link Between Data and Action

As finance automation M&A accelerates, AI-native decision engines are emerging as the connective tissue between data and execution systems. Beroe MAX powered by Kearney is framed as “the missing connecting layer between data and execution systems,” designed to make procurement continuously competitive by turning intelligence into timely, contextual decisions. Built on a neurosymbolic framework with agentic AI, MAX combines 30 million live market signals from Beroe with Kearney’s codified methodology and benchmarks, then applies them to an organization’s own spend, contracts, and suppliers. When tariffs change, commodity prices spike, or supplier risk scores move, the decision engine reassesses categories and flags actions before teams go hunting for insights. In the broader finance stack, this type of AI-native layer is what allows AP, AR, planning, and treasury systems to move from passive recordkeeping to proactive financial operations platforms that recommend and, increasingly, trigger execution.

Integrated Workflows: Where Finance Automation Meets Procurement

Consolidation is creating new opportunities to connect finance and procurement into shared, end‑to‑end workflows. On the finance side, acquisitions are pulling AP, AR, cash management, and spend analytics into unified platforms, reducing handoffs and data gaps around payments and working capital. On the procurement side, AI-native decision engines such as Beroe MAX powered by Kearney sit above category, sourcing, and contract tools to orchestrate decisions across cost, risk, and ESG. Procurement leaders face faster‑moving supply markets, but often with no extra headcount, which makes continuous intelligence and workflow integration more valuable than isolated insights. When combined, these trends point toward a single operating fabric where spend planning, sourcing, contracting, invoicing, and payment flow through one data model. That opens the door to automated policy enforcement, dynamic supplier choices, and real-time working capital decisions driven by a common view of risk and opportunity.

Platform vs. Point Solution: What CFOs and CPOs Must Decide Next

For enterprise buyers, the finance automation M&A wave narrows the vendor field but widens the feature sets, sharpening the trade‑off between point solutions and consolidated platforms. Integrated financial operations platforms promise simpler integration, consistent data models, and cross‑workflow AI—from AI procurement decisions to cash forecasting—at the cost of greater dependency on a few providers and their pricing power. Point solutions still appeal where a function needs leading‑edge depth, such as AP invoice capture or specialized risk analytics, but must be connected through APIs or an AI decision layer to avoid new silos. The launch of AI-native engines like Beroe MAX powered by Kearney hints at a hybrid path: keep some best‑of‑breed tools, but centralize intelligence and orchestration. CFOs and CPOs now need a reference architecture that decides where to standardize on platforms and where differentiated tools can justify added integration effort.