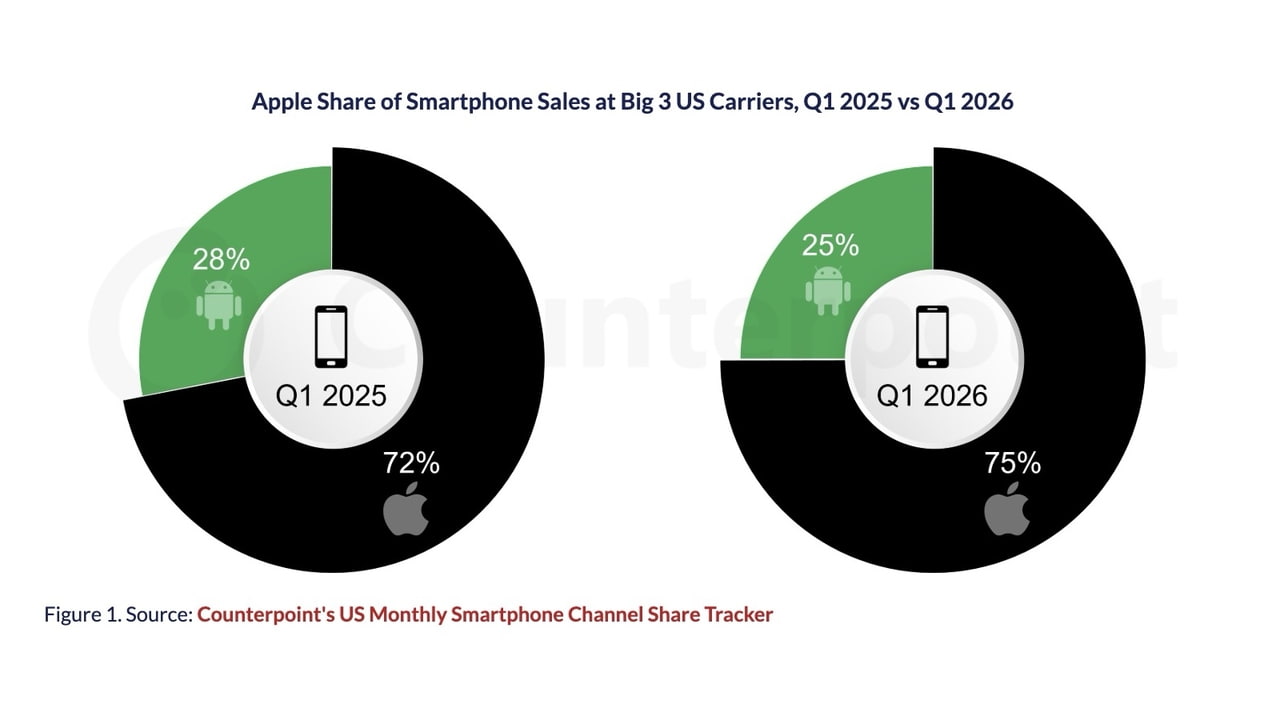

iPhone Sales Rise Against a Falling Smartphone Market

Apple delivered rare iPhone sales growth in the first quarter of 2026 even as the broader smartphone market contracted. According to Counterpoint Research, Apple iPhone sales growth reached 1.3% year over year in the period, while total smartphone shipments declined 5.7%. Android device sales were hit especially hard, dropping 14.4% as economic pressure and weaker upgrade cycles weighed on demand. Consumers in lower-end and prepaid segments pulled back on spending, often choosing to pay down debt instead of buying new devices. This divergence created a notable split: mainstream smartphone demand softened, yet Apple managed to expand its share at major carriers, reaching 77% of smartphone sales at Verizon. The result underscores how Apple’s performance was less about a booming market and more about capitalizing on specific pockets of demand and timing advantages within an otherwise sluggish Q1 2026 smartphone market.

Samsung Phone Delays Open a Window for Apple

A key factor behind Apple’s outperformance was not just its own products, but Samsung’s missteps. Samsung phone delays pushed the launch of the Galaxy S26 series from its typical January window to March 11, compressing its sales opportunity into the latter part of the quarter. Counterpoint Research notes that last year’s Galaxy S25 arrived earlier, giving Samsung more time to build momentum. This year, the gap created a vacuum in the premium Android segment. As senior analyst Tyler Graham observed, when one brand delays a flagship launch, it creates a window of opportunity—Apple stepped in decisively. With fewer fresh Android alternatives on shelves, premium buyers gravitated to the latest iPhone models, boosting Apple’s market share gains and helping it strengthen its position across carrier channels.

iPhone 17 Demand and Shifted Holiday Sales Fuel Momentum

Apple’s iPhone 17 lineup was the central engine of its Q1 performance. Counterpoint Research points to strong iPhone 17 demand as the primary driver of Apple iPhone sales growth, aided by supply constraints late last year that pushed some holiday purchases into the new quarter. Apple itself described a “historic” holiday season for iPhone, and that strength spilled into the March quarter. The base iPhone 17 proved more popular than anticipated, forcing Apple to adjust production to keep up. This combination of delayed fulfillment and ongoing enthusiasm gave Apple a smoother demand curve while competitors struggled with softer consumer interest. With fresh hardware, a broad carrier promotion push, and an established ecosystem, Apple turned what could have been a post-holiday lull into another growth phase for its flagship devices.

Pricing Strategy and the Role of the iPhone 17e

Apple’s pricing choices further reinforced its advantage. The iPhone 17e, positioned as Apple’s entry-level smartphone, maintained the same starting price as its predecessor while doubling base storage to 256GB. This move aligned with Apple’s strategy of expanding its ecosystem and boosting services revenue, even if it meant accepting thinner hardware margins. At the same time, rising memory costs pushed many manufacturers to raise prices or cut value. Samsung increased the price of its Galaxy S26 base and Plus models and removed its lower-storage entry option, making its lineup relatively less accessible. In contrast, Apple’s decision to hold the line on pricing while enhancing storage made the iPhone 17e particularly compelling. Combined with aggressive carrier promotions, this approach made it harder for Android brands to match Apple’s perceived value proposition during a challenging Q1 2026 smartphone market.

Strategic Advantage Beyond Product Innovation

Apple’s recent market share gains highlight how strategic timing and competitor errors can be as important as product innovation. While the iPhone 17 family is clearly resonating with buyers, much of Apple’s edge in early 2026 stems from how effectively it capitalized on Samsung phone delays and a disrupted Android launch cycle. The company benefited from shifted holiday demand, maintained pricing for the iPhone 17e, and leveraged carrier subsidies to keep iPhone 17 demand strong. Meanwhile, broader market weakness—particularly in prepaid and low-end segments—hit rivals harder than Apple. The lesson for the industry is that success in smartphones now depends as much on launch cadence, pricing discipline, and supply management as on feature lists. In this environment, Apple’s ability to execute when competitors stumble is emerging as a strategic weapon, positioning it strongly for further market share gains if these dynamics persist.