iPhone Sales Growth in Q1 2026 Against a Shrinking Market

Apple’s iPhone sales growth in Q1 2026 stood out sharply against a contracting smartphone market. According to Counterpoint Research data cited in multiple reports, iPhone sales volume rose 1.3% year over year even as overall smartphone shipments declined 5.7%. Android devices were hit much harder, with a 14.4% drop over the same period, underlining how uneven the downturn has been. The iPhone 17 family remains the key engine behind Apple’s resilience. Launched in September, the line continued momentum from a “historic” holiday quarter into the March period, helped by supply constraints late last year that pushed some demand into Q1. This outperformance in iPhone sales growth Q1 2026 did more than offset weakness in prepaid and low-end segments, where consumers under economic pressure chose to delay upgrades and prioritize paying down debt instead.

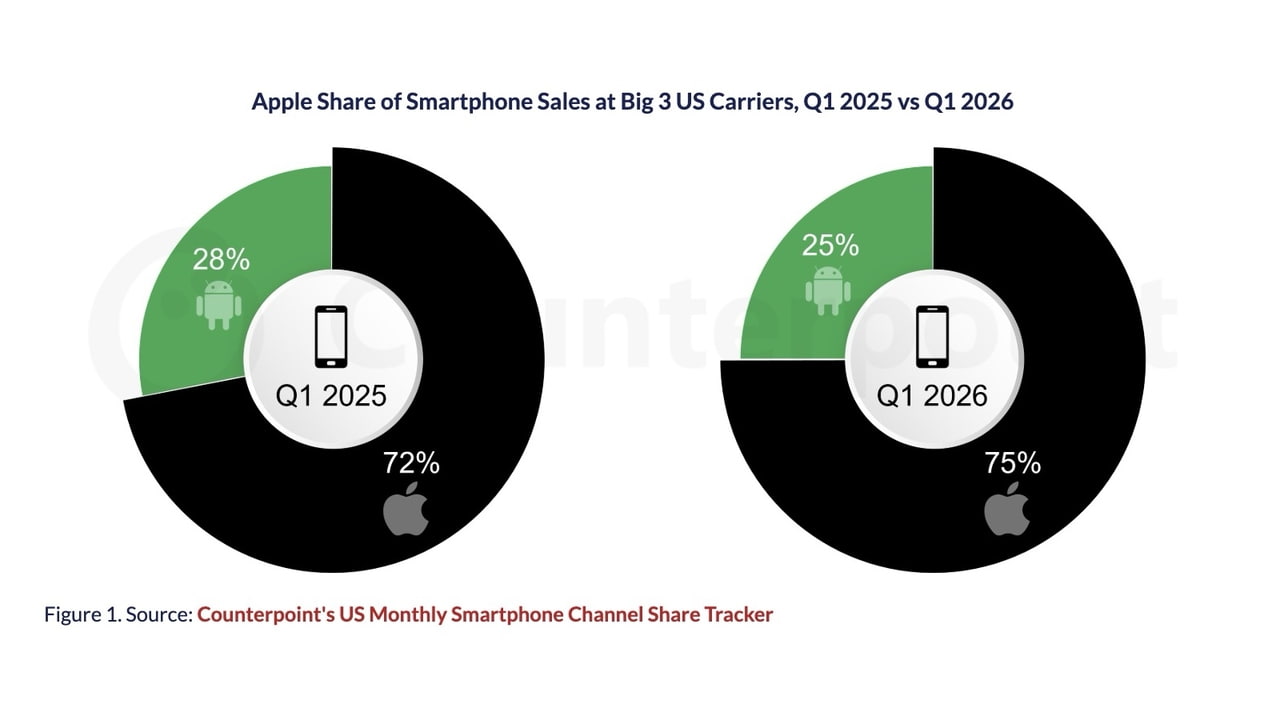

Samsung’s Launch Delays Gave Apple a Crucial Opening

Timing played an outsized role in smartphone market competition. Samsung’s Galaxy S26 series, normally unveiled in January, did not arrive until March 11. That pushed its key launch window deep into the quarter and gave Apple several weeks with effectively no fresh flagship challenge. Counterpoint analysts note that when one brand delays a major release, it creates a vacuum that competitors can exploit—and Apple moved quickly to fill it. The result was share gains across major carriers, including a commanding 77% of smartphone sales at Verizon. Samsung’s strategy further diverged on pricing and configuration. The company raised prices for its base and Plus Galaxy S26 models and removed the 128GB entry configuration, even as memory costs climbed. Those choices contrasted sharply with Apple’s approach and magnified the impact of Samsung’s delays in the Apple vs Samsung delays storyline.

Apple’s Pricing Strategy and Ecosystem Play

Apple’s pricing decisions around the iPhone 17 lineup have been central to its recent gains. The iPhone 17e, positioned as the entry model, retained its USD 599 (approx. RM2,760) starting price from the previous generation while doubling base storage to 256GB. This move aligns with Apple’s long-term focus on expanding its ecosystem and boosting services revenue rather than maximizing near-term hardware margins. Combined with aggressive carrier promotions, this strategy makes it harder for Android brands to match perceived value without sacrificing profitability. Counterpoint suggests that if Apple can avoid significant price increases despite rising component costs and continue outspending rivals on promotions, it will be difficult for Android OEMs to keep pace. In effect, Apple is turning stable pricing and richer configurations into a competitive moat in an environment where many rivals are being forced into price hikes or feature compromises.

Mobile DRAM Price Impact on Production and Product Mix

Beneath the surface of headline sales numbers, the mobile DRAM price impact is reshaping how smartphones are designed and produced. TrendForce data shows contract prices for LPDDR4X are forecast to rise 70–75% quarter-on-quarter in 2Q26, with LPDDR5X up 78–83%. These steep increases follow several quarters of gains and now directly influence bill-of-materials decisions, especially for Android makers that compete heavily on price. Some vendors may struggle to fulfill long-term memory procurement commitments signed before the latest spikes. As a result, memory configurations are being trimmed: 12GB is becoming the mainstream high-end spec, 8GB the core mid-range, and 4GB common in entry devices. Although average DRAM content per phone is still expected to climb to 8.5GB this year, the pressure is greatest on low-end models where margins are thin and every additional gigabyte erodes profitability.

Supply Chain Pressures Are Redrawing Competitive Lines

Combined with weaker consumer demand, supply chain disruptions and component inflation are forcing a reset in smartphone market competition. Rising DRAM and NAND prices are squeezing low-cost Android manufacturers, making it harder to sustain sub-premium models while offering competitive specifications. Analysts expect fewer ultra-low-cost phones, more modest memory configurations at existing price points, and greater reliance on software optimization and cloud services to compensate for local memory limitations. In this environment, larger players with stronger balance sheets and integrated ecosystems—such as Apple and Samsung—are relatively better positioned. Apple’s ability to maintain stable iPhone pricing so far, despite signaling “significantly higher memory costs” in the near term, highlights this advantage. As smaller brands retrench and major vendors rethink product portfolios, the balance of power in the smartphone market may tilt even further toward premium devices and ecosystem-driven strategies.