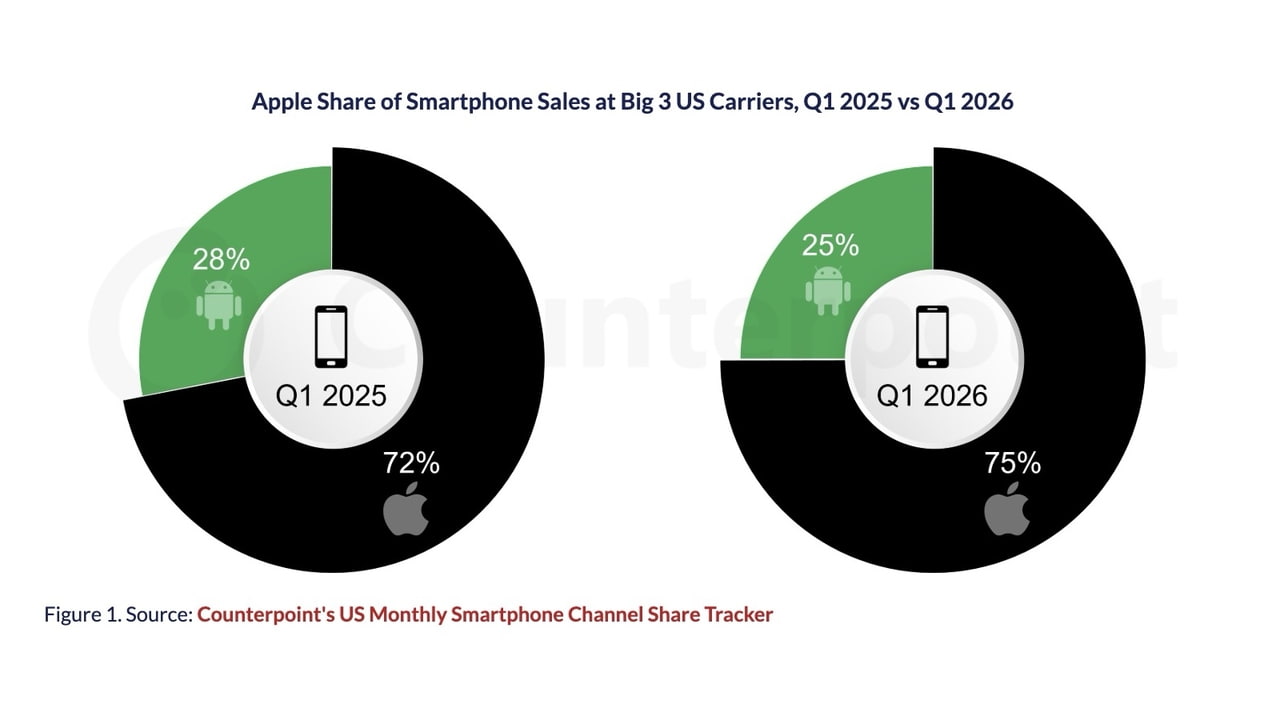

iPhone Sales Rise Against a Falling Market

Apple achieved rare smartphone market share gains in the first quarter of 2026, even as overall demand contracted. Counterpoint Research data shows iPhone sales volume growing 1.3% year over year, while total smartphone shipments declined 5.7%. Android devices bore the brunt of the downturn, with sales falling 14.4% over the same period. This divergence underscores Apple’s growing resilience: instead of merely weathering the slowdown, it expanded its footprint at major carriers, reaching as high as 77% of smartphone sales at Verizon. Analysts point to a mix of pent‑up demand, strategic pricing, and brand strength to explain the outperformance. While many competitors struggled with softer upgrades and macroeconomic pressure on lower-end buyers, Apple’s premium portfolio and ecosystem kept users upgrading, reinforcing its trajectory toward greater Apple market dominance 2026 and reshaping expectations for the rest of the year.

iPhone 17 Demand Turned Supply Friction into Sales Momentum

The iPhone 17 lineup sits at the heart of Apple’s recent iPhone 17 sales growth. Supply constraints in late 2025 pushed a portion of holiday demand into the March quarter, turning what could have been a weakness into an extended sales runway. Counterpoint notes stronger-than-expected interest in the base iPhone 17, forcing Apple to recalibrate production to keep up. Apple itself described a “historic” holiday quarter for iPhone demand, followed by 22% growth in iPhone unit sales into the March period, indicating sustained appetite rather than a one-off spike. This product cycle shows how Apple is increasingly adept at smoothing demand over multiple quarters, maintaining buzz and availability long after launch day. By keeping the iPhone 17 family front and center in carrier promotions, the company amplified upgrade intent, further widening the gap in the iPhone vs Samsung competition during a critical sales window.

Samsung’s Delayed Flagship Opened a Window for Apple

While Apple executed smoothly, Samsung inadvertently handed its rival extra room to run. The Galaxy S26 series, usually unveiled in January, did not arrive on shelves until March 11, later than the typical schedule that saw the Galaxy S25 go on sale in February. That delay left a conspicuous gap in the premium Android segment just as upgrade-minded users were shopping. Counterpoint’s senior analyst Tyler Graham noted that when one brand delays a flagship, it “opens a window of opportunity to fill that vacuum” – and Apple did exactly that. With the iPhone 17 already well established in the market, Apple captured buyers who might otherwise have waited for Samsung’s latest release. The timing misalignment didn’t just dent Samsung; it tilted overall smartphone market share toward Apple, especially at carriers where premium devices drive outsized visibility and marketing support.

Pricing Strategy and Entry Models Tighten Apple’s Grip

Apple’s pricing approach around the iPhone 17e further reinforced its edge. The company held the entry model at USD 599 (approx. RM2,760), matching the previous generation’s starting price, while doubling the base storage to 256GB. This move signaled a willingness to trade some short-term hardware margin for ecosystem expansion and future services revenue. In contrast, Samsung raised prices on its Galaxy S26 base and Plus models by USD 100 (approx. RM460) compared with the prior lineup and phased out its 128GB entry option, even as memory costs climbed. The result: Apple’s offer looked more compelling to value-conscious premium buyers, particularly when combined with strong carrier promotions. Counterpoint argues that if Apple can maintain this pricing discipline and continue outspending rivals on promotions, Android manufacturers will find it increasingly difficult to keep pace in both volume and perceived value.

Industry Slowdown Highlights Apple’s Relative Strength

Beyond flagship timing and pricing, the broader smartphone industry faced real headwinds. Analysts observed unexpected weakness in prepaid and low-end segments, as many consumers chose to use tax refunds to pay down credit card balances rather than upgrade phones. Rising memory costs compounded the pressure, squeezing smaller brands out of the budget tier and allowing a handful of players like Motorola and Samsung to consolidate share in prepaid channels such as Cricket and Metro. Yet even in this environment, Apple’s premium-focused strategy and cohesive ecosystem kept upgrade demand steady. The company grew iPhone sales while the market contracted, underscoring a widening gap between its performance and that of the wider industry. As economic pressures persist, Apple’s combination of disciplined pricing, strong iPhone 17 sales growth, and smart timing against competitor delays positions it to extend its market lead in the coming quarters.