Four Memory Spikes Since NAB: Why Blackmagic Prices Keep Climbing

Blackmagic Design has announced another Blackmagic price increase across its URSA Cine cameras, Cloud Store systems, Media Modules, and ATEM and HyperDeck models that ship with built‑in storage. In a briefing to dealers, the company pointed directly to flash memory and DRAM costs, which have reportedly surged four times since NAB. The core problem: Blackmagic is competing for the same enterprise‑grade flash and high‑speed DRAM that data centers are buying aggressively for AI training clusters. That demand has tightened NAND flash, high‑speed DRAM, and even mature‑node components across the market, turning what once looked like a temporary flash memory shortage into an ongoing structural squeeze. After absorbing the first waves internally, Blackmagic is now passing increases through to customers, signalling that it no longer expects quick relief. For production teams, this is not a one‑off anomaly but a warning that cinema equipment costs linked to solid‑state storage may remain volatile.

URSA Cine Pricing: From Aggressive Cuts to a Full‑Circle Rebound

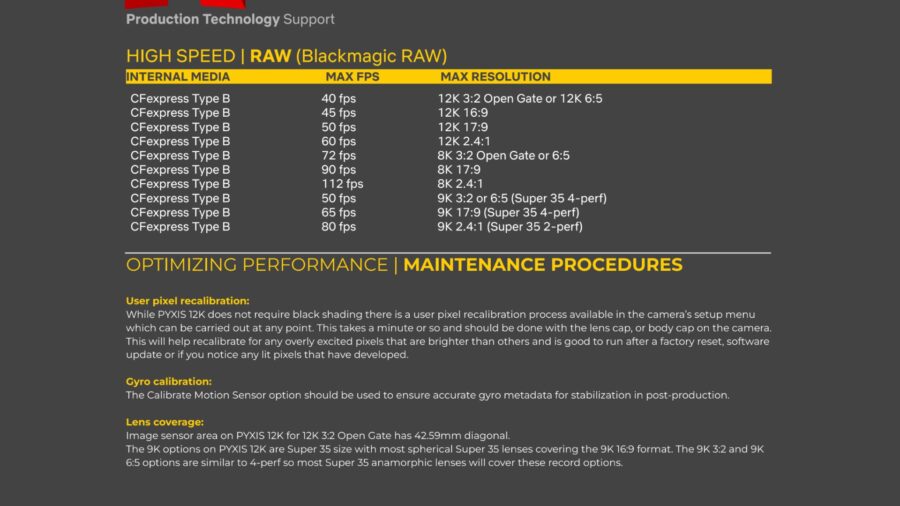

Nowhere is the new pricing reality clearer than in URSA Cine pricing. The URSA Cine 12K LF kit launched at USD 14,995 (approx. RM69,000) and was later cut to USD 9,495 (approx. RM43,700) as manufacturing efficiencies kicked in. Since then, the same camera has climbed back to USD 11,995 (approx. RM55,200), and with the latest adjustment it now sits at USD 15,495 (approx. RM71,400), above its original launch price. The matching EVF kit has followed a similar trajectory, jumping from USD 13,495 (approx. RM62,200) to USD 16,795 (approx. RM77,300). At the same time, Blackmagic continues to push lower‑cost options like the modular PYXIS 12K, which delivers a Netflix‑approved 12K sensor in a box‑style body at USD 5,495 (approx. RM25,300). The contrast underscores a new tension: high‑end, memory‑dense flagships are getting pricier just as more affordable, approved alternatives enter the ecosystem.

Storage Products Take the Hardest Hit—and Reshape Post‑Production Budgets

While cameras attract the headlines, the steepest pressure is hitting storage‑centric products that embody the flash memory cost problem. Blackmagic’s Cloud Store line is essentially high‑performance M.2 RAID in a network chassis, and its Media Modules are M.2 SSD packs designed to live inside URSA Cine bodies. Because these devices are dominated by enterprise‑grade NAND and DRAM, any spike in component pricing translates almost directly into higher cinema equipment costs. The latest round of increases hits higher‑capacity Cloud Stores hardest, reflecting how memory‑per‑box magnifies the production budget impact. For post‑production teams, this is more than a marginal nuisance. Centralized shared storage, on‑set backup, and nearline archives all depend on fast flash, so each incremental rise compresses room for additional grading workstations, VFX nodes, or backup tiers. In effect, storage is becoming the new choke point that can quietly dictate the real scope of a project’s finishing pipeline.

From Set to Stream: Acquisition and Workflow Choices Under Pressure

The latest Blackmagic price increase reaches across both acquisition and live or collaborative workflows, touching URSA Cine bodies, ATEM switchers with internal storage, and Cloud Store appliances. For camera departments, higher URSA Cine pricing complicates own‑versus‑rent equations and may nudge some productions toward the more affordable, Netflix‑approved PYXIS 12K. That body delivers the same full‑frame 12K RGBW sensor as the URSA Cine 12K LF while recording to CFexpress Type B cards, which are themselves exposed to the same memory volatility. On the workflow side, rising costs for integrated storage mean that decisions about live switching, on‑set review, and remote collaboration are now tightly bound to flash prices. Teams planning multi‑camera, high‑resolution capture must weigh whether to centralize on Cloud Store‑style systems or spread risk across smaller, modular storage nodes, knowing that every terabyte of high‑speed flash now carries a premium that could otherwise fund lenses, crew days, or additional units.

Strategic Responses: How Production Teams Can Rethink Capex

With flash memory costs reshaping cinema equipment costs, production companies need to revisit capital expenditure strategies rather than treating each price swing as an isolated shock. One approach is to decouple high‑value sensors from fixed storage where possible, favoring cameras that lean on interchangeable media and shifting long‑term investment toward flexible, modular storage infrastructure. Another is to diversify acquisition formats—using the URSA Cine or PYXIS 12K for hero shots while mixing in lower‑data‑rate options for coverage—to reduce the pressure on both camera media and shared storage. Crucially, budget planning should now assume that memory‑heavy gear will see periodic repricing, with contingency lines earmarked specifically for storage and media. In this environment, conversations about camera choice, switching, and archiving are no longer independent; they are all downstream of the same flash memory shortage dynamics that are likely to persist as AI data centers continue to outbid traditional media customers.