Chokepoints Turn from Map Features into Strategic Liabilities

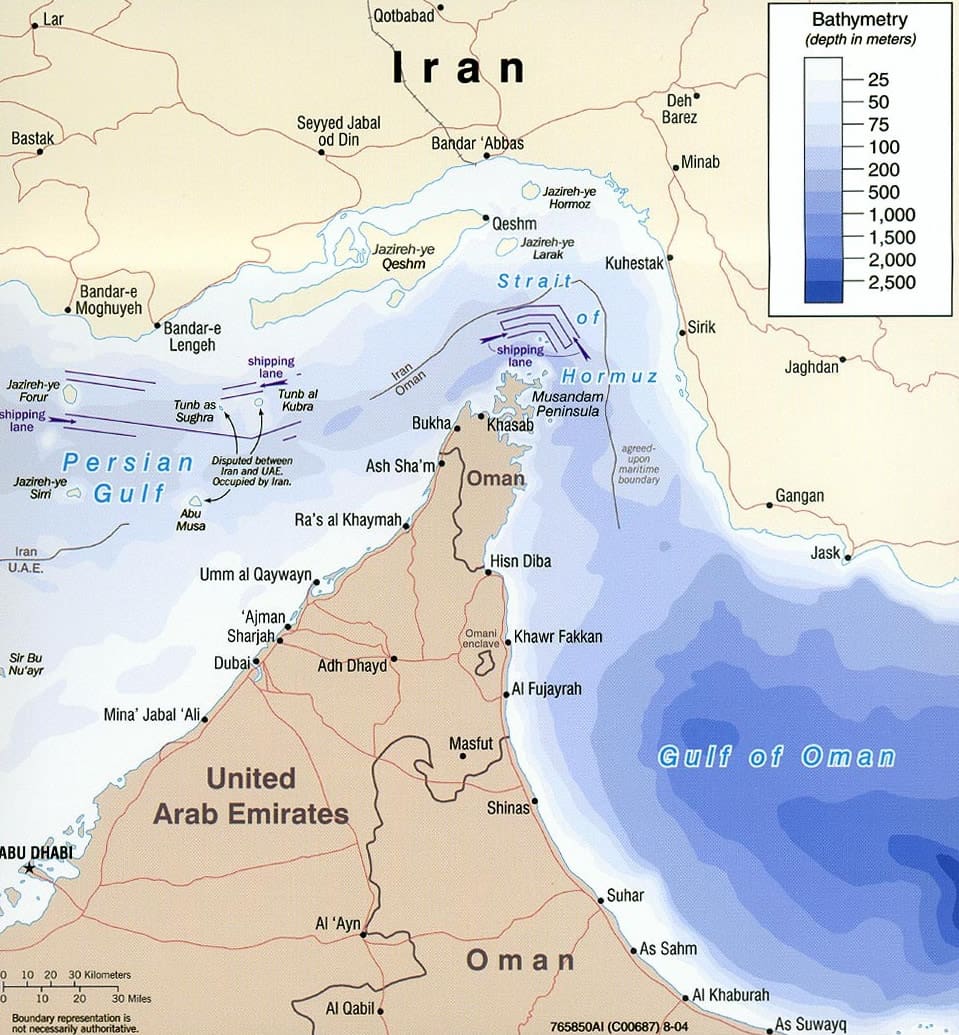

Energy supply chain risk is no longer an abstract geopolitical discussion; it is reshaping how companies design networks and allocate capital. The Strait of Hormuz illustrates the problem. A large share of seaborne oil moves through this narrow corridor, making it not just a regional security issue but a structural dependency embedded in global sourcing strategies and transportation plans. Recent instability has reinforced a pattern seen with pandemic disruptions, war-related sanctions, Red Sea diversions, and port congestion: when too much volume flows through too few nodes, a single incident can cascade into global geopolitical supply disruption. As those assumptions about reliability weaken, the economics of energy logistics change. Routes that once looked optimal on a cost-only basis now appear fragile once exposure and recovery time are factored in. For energy companies and their customers, chokepoint risk has become a core network design issue rather than a background concern.

Diversifying Routes and Storage to Reduce Exposure

In response, energy firms and governments are diversifying routes and stockpiles to build supply chain resilience. One example is the deepening collaboration between a major energy importer and the UAE on expanded crude supply and joint stockpiles. The goal is to secure more flexible access to crude and increase storage in the importing country, creating a buffer when chokepoints are threatened. Fujairah, connected by pipeline and located outside the Strait of Hormuz, is central to this logic because it offers an alternative export path that bypasses a vulnerable corridor. The port does not eliminate regional risk, but it provides routing optionality that can stabilize flows and pricing when traditional lanes are constrained. This shift shows how ports, pipelines, and storage terminals gain strategic value when they reduce dependency on single routes and give buyers time and room to maneuver during disruptions.

Infrastructure Investments Reorient Around Alternative Corridors

Energy infrastructure planning is increasingly driven by risk-adjusted returns rather than pure throughput or cost metrics. ADNOC’s planned AED200 billion, roughly USD 55 billion (approx. RM253 billion), in project awards from 2026 through 2028 signals how capital is being deployed across the value chain to enhance flexibility. While these are energy investments on the surface, they are equally supply chain infrastructure bets: expanding production capacity, storage terminals, and export options that can keep flows moving if a primary route is compromised. Assets tied to locations like Fujairah become more valuable because they sidestep chokepoints and diversify export pathways. This is how supply chain geography typically changes—not through one dramatic relocation, but through repeated disruptions that reprice existing assets. Ports that avoid congested corridors, pipelines that offer route diversity, and storage that extends decision time all become central to long-term energy supply chain risk management.

From Lowest-Cost Networks to Risk-Adjusted Supply Chains

For decades, energy logistics were designed around efficiency: lowest landed cost, high asset utilization, and lean inventories. That approach assumed stable trade lanes and broadly reliable energy flows. Today, war, political coercion, piracy, cyber threats, and infrastructure bottlenecks make that assumption untenable. Companies are moving toward risk-adjusted network design, where cost is evaluated alongside exposure, substitutability, and recovery time. A low-cost route that depends on a single chokepoint may prove far more expensive once disruption probabilities are considered. In practical terms, this means placing a tangible value on alternate routes, backup suppliers, additional inventory, and flexible capacity. Energy is treated as a strategic variable in network design, influencing decisions on plant locations, cold chains, and data centers. Supply chain resilience is no longer a premium feature; it is a core design principle that shapes how energy-intensive industries choose where and how to operate.

Embedding Geopolitical Risk into Supplier and Technology Decisions

The shift also changes how companies evaluate suppliers and technology. Traditional supplier risk programs focused on financial health and delivery performance, but often ignored geographic dependencies and chokepoint exposure. A vendor may appear strong operationally yet still rely on a vulnerable port, energy source, or corridor that exposes the buyer to geopolitical supply disruption. Modern supplier scoring increasingly incorporates trade-lane exposure, energy dependency, and political risk. At the same time, technology must connect external risk signals to internal decisions. ERP, TMS, WMS, and planning tools each manage part of the operating model, but chokepoint disruptions cut across them all—impacting fuel costs, production schedules, procurement, inventory, and customer commitments. The companies best positioned for the new environment will be those that can quickly translate external geopolitical shocks into coherent adjustments across their entire energy supply chain and operating network.