How a 3D printer IPO wave is redefining market maturity

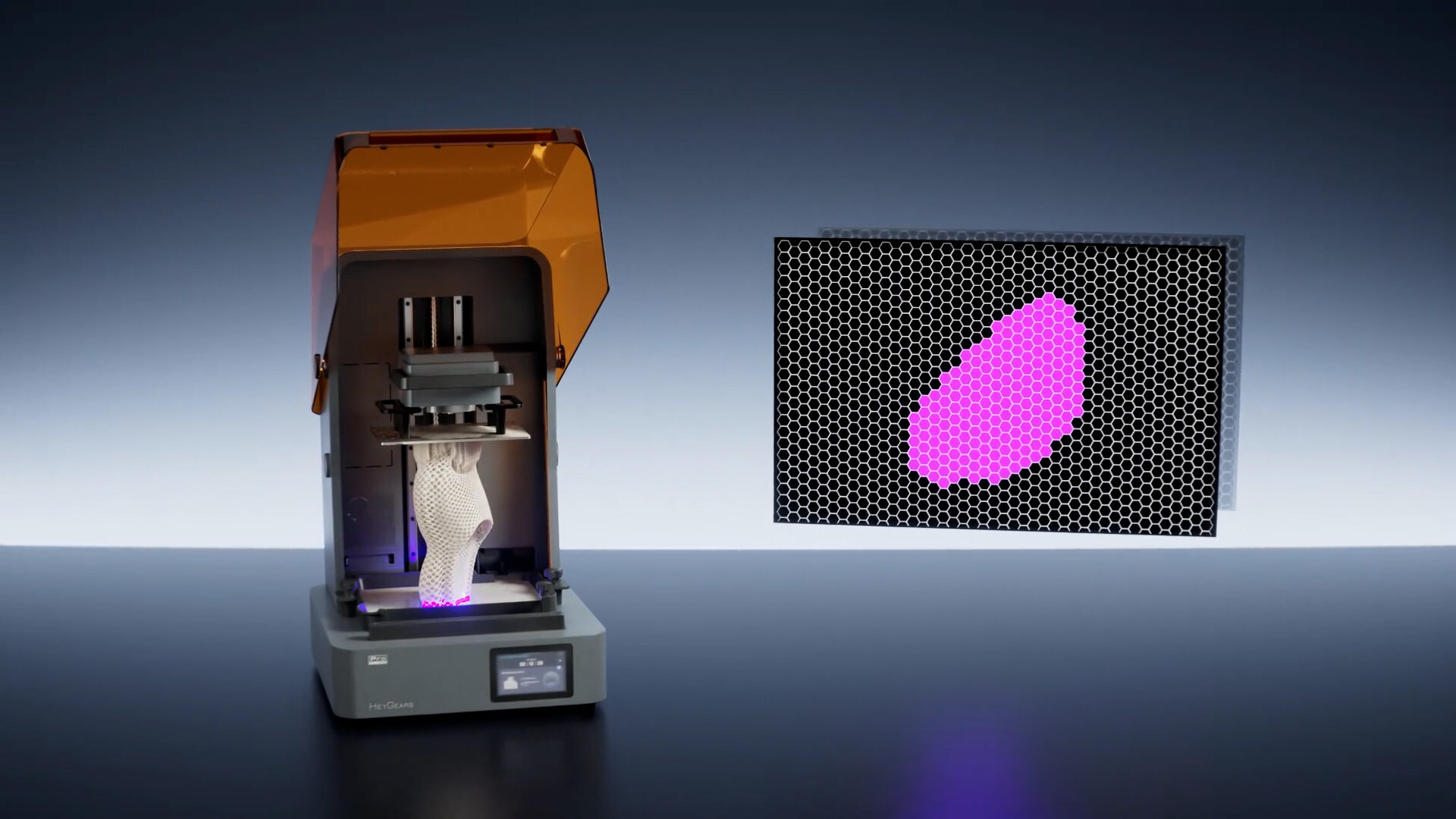

The current wave of 3D printer IPO and fundraising activity in Asia refers to a fast‑accelerating shift from small‑scale prototyping and hype‑driven demonstrations toward capital‑intensive, production‑grade additive manufacturing platforms backed by public markets and institutional investors. Creality’s public offering on the Hong Kong Stock Exchange has become the clearest signal of this shift, positioning a desktop 3D printer specialist as a listed technology stock. The company raised about HK$1.27 billion, with its public offer 3,829 times oversubscribed, demonstrating strong investor appetite for the APAC additive manufacturing story. At the same time, resin specialist HeyGears secured USD 44 million (approx. RM202 million) in a Series C round to move deeper into consumer systems and materials. Together, these deals show that capital deployment is now focused on scaling production, broadening product lines and building recurring revenue around materials rather than on one‑off machine sales.

Desktop 3D printer leaders rush toward public markets

Desktop 3D printer makers are at the front of the public‑market queue, using listings to fund global expansion. Creality’s Hong Kong debut under the code 3388 sets a reference point for the entire segment, as it becomes the first consumer 3D printing company traded there. Its oversubscribed 3D printer IPO signals that retail and institutional investors now see desktop 3D printer brands as scalable hardware‑plus‑materials platforms rather than hobbyist suppliers. Filament producer Sunlu Technology is also preparing for a listing shift, moving from the New Third Board toward a ChiNext IPO to finance capacity expansion. Meanwhile, Bambu Lab is building retail reach by placing printers in 64 Sam’s Club stores and teasing its A2L large‑format model. This combination of market listings and channel expansion shows how capital is being used to lock in brand position before the next phase of 3D printing market expansion.

Metal powders, lasers and wire‑arc systems scale for demand

Beyond desktop systems, metal additive manufacturing is attracting heavy investment in both powders and equipment. Tiangong International is scaling plasma‑atomized titanium alloy powder toward a 3,000‑tonne‑per‑year target, underlining expectations of steady demand from aerospace, industrial and high‑performance sectors. Shenzhen Gongda Laser closed a Series C of several hundred million yuan, planning to expand its green‑laser metal AM business from more than 100 deployed systems to 1,000 within three years, focused on copper thermal‑management parts for AI compute hardware. According to 3DPrint.com reporting, Gongda’s Xihe subsidiary views this as a path to serial production volumes rather than niche prototyping. In Japan, DAIHEN entered the metal printing space with ArcBuilder3D, a wire‑arc system claimed to cut costs to less than half those of powder‑based methods, priced at 75 million yen and targeting large structures such as ship propellers and rocket nozzles.

Defense, medical and consumer uses anchor APAC additive manufacturing

Defense and medical programs are turning APAC additive manufacturing into a diversified production ecosystem. In Korea, DN Solutions’ AM2CNC platform is heading into serial defense production, while LinkSolution has demonstrated a mobile AM Fab container for field‑ready drone and spare‑parts printing. Medical applications are moving from lab work to preclinical and pilot stages: Rokit Healthcare’s omentum‑based kidney patch showed improvements in kidney function and fibrosis, and T&R Biofab is helping lead a government‑backed AI bioink project to reduce variability in organ‑specific printing. On the consumer side, resin and powder processes are reshaping footwear, with TPM3D’s SLS PEBA shoes passing a 200,000‑cycle flex test and Decathlon’s Kiprun KIPNEXT running shoe using an HP Multi Jet Fusion midsole. These varied projects show APAC additive manufacturing evolving beyond machines into anchored end‑use markets, a key foundation for long‑term 3D printing market expansion.

APAC additive manufacturing emerges as a global production hub

Taken together, these IPOs and capital raises show APAC additive manufacturing consolidating into a global hub for both innovation and manufacturing scale. Capital deployment is outpacing trade‑show announcements, with funds flowing into higher‑volume powder lines, larger machine fleets and AI‑assisted production platforms such as Unionfab’s extended metal printing service in the United States, Canada and Germany. Companies are investing not only in hardware, but also in materials and software that shorten lead times from weeks to days. The region’s ecosystem now spans consumer desktop 3D printers, industrial metal systems, bioprinting platforms and 4D‑printed medical devices. As more 3D printer IPO events reach public markets and secondary offerings recycle capital into expansion, APAC stands poised to define the next decade of global additive manufacturing, with listed companies acting as anchor tenants for a wider supply‑chain and applications network.