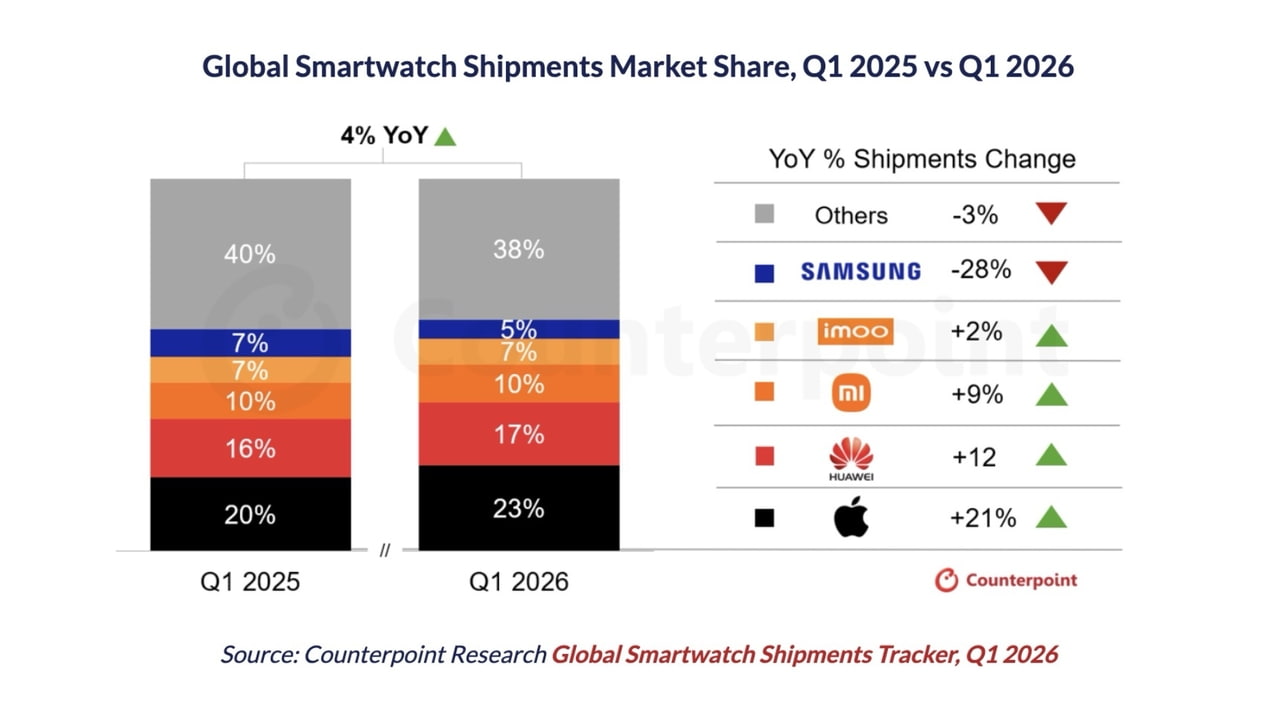

Apple’s 23% Share Redefines the Smartwatch Landscape

Apple’s expanding share of global smartwatch shipments in Q1 2026 describes a market where one premium player is capturing nearly all growth while key Android rivals shrink. The company’s Apple Watch shipments increased 21% year over year, pushing its global market share to 23%, up from 20% a year earlier. Over the same period, the overall smartwatch market grew only 4%, meaning Apple’s gains far outpaced the sector. According to Counterpoint Research, Apple’s growth rate was the fastest among the top 10 smartwatch brands. This performance highlights how the Apple Watch market share is being driven by strong demand for both flagship and mid-range models, in contrast to weaker results from other brands. As a result, Apple is not only holding its lead but expanding it in a market that is growing slowly.

Samsung Galaxy Watch Decline and Market Share Erosion

While Apple expanded, Samsung’s smartwatch shipments fell 28% year over year in Q1 2026, cutting its global share from 7% to 5%. This sharp decline means Samsung not only missed out on the 4% overall wearable market growth but moved in the opposite direction, giving up ground in a segment where it was once the main challenger to Apple. The current Galaxy Watch lineup, led by the Galaxy Watch 8, remains limited to 4G LTE support, while Apple’s 2025 Watch range already supports 5G. Rumors suggest the upcoming Galaxy Watch Ultra 2 may add 5G, but it is unclear whether standard Galaxy Watch 9 models will match that capability. Until the refreshed devices arrive, Samsung’s smartwatch shipments Q1 2026 underline how quickly momentum can swing away from a brand that lacks timely upgrades.

Premium Features, Health Tracking and Changing Consumer Preferences

The split between Apple’s growth and Samsung’s decline points to a shift toward premium smartwatches with advanced health and connectivity features. Counterpoint Research notes that the Apple Watch Series 11 and budget-friendly Watch SE 3 drove Apple’s 21% shipment increase, with improved sensors and health-tracking tools attracting first-time buyers. The entire 2025 Apple Watch lineup supports 5G, positioning it as a future-ready option for consumers who see their smartwatch as a core health and communication companion. At the same time, the average selling price of smartwatches rose 6% in Q1 2026, driven by demand for advanced health monitoring, AI functions, and satellite connectivity. As more users upgrade from basic fitness bands to full smartwatches, brands that pair premium hardware with meaningful health insights are best placed to benefit.

Chinese Brands Rise as Huawei and Xiaomi Gain Ground

Beyond the Apple–Samsung contrast, Chinese brands helped offset Samsung’s weakness and reshaped competitive dynamics. Huawei increased its global smartwatch share from 16% to 17%, while Xiaomi recorded 9% shipment growth. Huawei holds about 40% of its home smartwatch market, which itself grew 15% year over year, giving the company a powerful base from which to expand internationally. These gains show that while the Apple Watch market share leads at the premium end, there is intense competition in mid-range and regionally focused segments. For Samsung, this means pressure from both sides: Apple dominates the high-end category, while Huawei, Xiaomi, and other Chinese brands capture cost-conscious buyers who still want capable health and connectivity features. If Samsung cannot stabilize shipments after its next releases, the gap with Apple could widen further as Chinese makers consolidate their regional strength.

Outlook: Slow Market, Concentrated Growth, and AI-Driven Upside

Despite the headline swings, the smartwatch market remains a slow-growth category, with Counterpoint projecting a compound annual growth rate of 3% through 2030. This modest pace makes Apple’s Q1 2026 performance more striking, as it captured nearly all of the 4% wearable market growth while Samsung registered a steep shipment decline. Rising average selling prices suggest that consumers are willing to pay more for advanced health metrics, AI-powered insights, and satellite communication, rather than basic notifications and step counting. Component shortages in RAM and memory could weigh on volumes later in 2026, but analysts expect the impact to be milder than in laptops and smartphones, because premium wearables carry healthier margins and lower materials costs. The next test will come in the second half of the year, when Samsung’s refreshed Galaxy Watch lineup shows whether it can reclaim share from Apple and fast-rising Chinese competitors.