iPhone 17 Sales Growth Amid a Shrinking Market

Apple’s latest flagship managed to grow iPhone 17 sales growth even as the broader industry contracted. In the first quarter of 2026, iPhone sales volume rose 1.3% year over year, while overall smartphone market share Q1 2026 declined by 5.7%. Android device sales were hit even harder, falling 14.4% over the same period. Counterpoint Research attributes much of Apple’s resilience to the iPhone 17 lineup, which continued to draw robust demand after a “historic” holiday season. Supply constraints late in the previous year pushed some purchases into the new quarter, particularly for the standard iPhone 17, which performed better than Apple initially expected. This combination of carried-over demand and a strong flagship portfolio allowed Apple market dominance to expand at a time when many competitors struggled to simply maintain their existing sales levels.

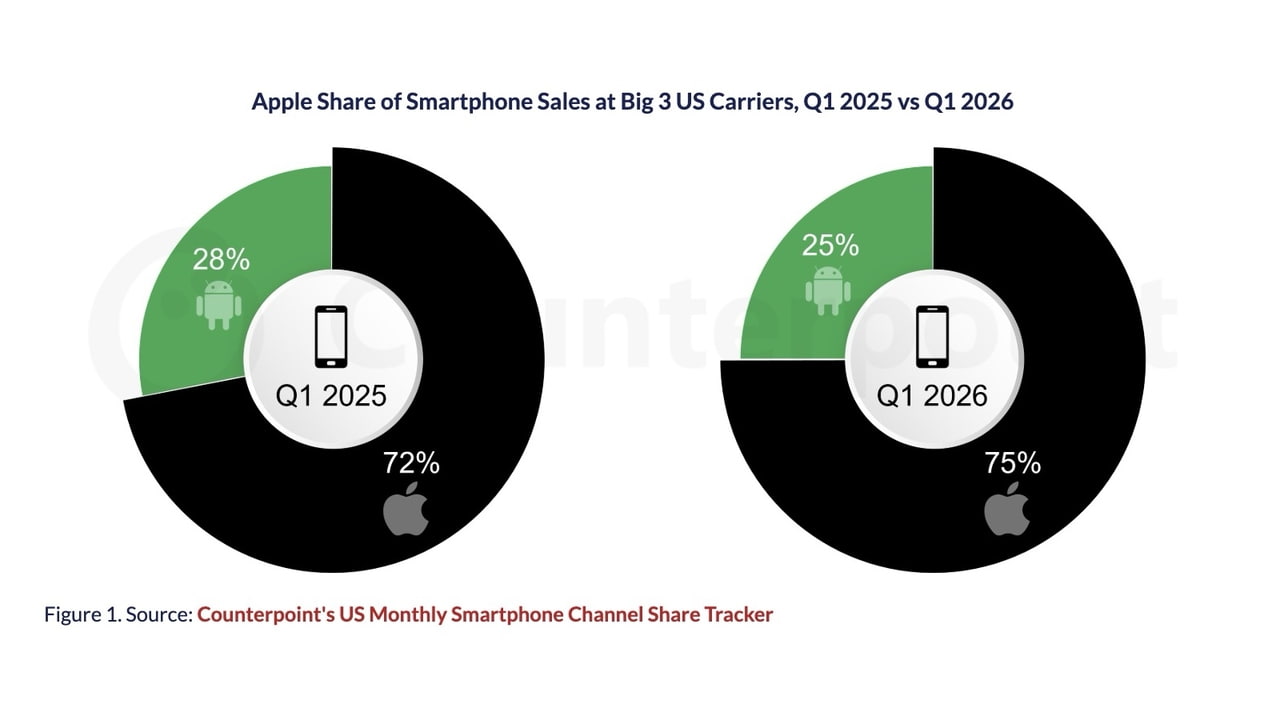

Samsung Launch Delays Opened a Competitive Vacuum

Samsung launch delays played a pivotal role in reshaping smartphone market share Q1 2026. Traditionally, Samsung rolls out its Galaxy S series early in the year, but the Galaxy S26 family slipped from a typical January debut to a March 11 launch. That shift effectively ceded several weeks of the premium segment to Apple. Counterpoint Research notes that when a major brand postpones a flagship release, it creates a vacuum that others can fill, and Apple moved quickly to capitalize. With iPhone 17 already in full swing, Apple captured buyers who might otherwise have waited for Samsung’s latest model. The impact was visible at major carriers, where Apple’s share climbed significantly, including reaching 77% of smartphone sales at one leading operator. In a market already under pressure, Samsung’s timing misstep amplified Apple’s advantage.

Pricing Strategy and the iPhone 17e Advantage

Beyond timing, Apple strengthened iPhone 17 sales growth with a disciplined pricing strategy anchored by the iPhone 17e. The entry-level model maintained the same starting price as its predecessor while doubling base storage to 256GB, enhancing perceived value without sacrificing accessibility. This approach supports Apple market dominance by prioritizing ecosystem expansion and services revenue, even if it compresses near-term hardware margins. In contrast, Samsung raised prices on its Galaxy S26 base and Plus models by USD 100 (approx. RM460) and removed its 128GB entry option, a tough move in an environment of rising memory costs and cautious consumers. With many buyers prioritizing debt repayment over upgrades, Apple’s mix of stable pricing and richer specs—backed by aggressive carrier promotions—made its devices comparatively more attractive. Counterpoint suggests that if Apple continues to hold the line on prices, Android rivals will face mounting pressure.

Weakness in Budget Segments Boosted Premium Leaders

While flagship launches grabbed headlines, underlying demand in the lower tiers further tilted the field toward Apple and a few large Android brands. Analysts observed notable softness in prepaid and low-end smartphone segments. Consumers who might typically use tax refunds to upgrade instead chose to pay down credit card balances amid broader economic uncertainty. Simultaneously, rising memory prices squeezed smaller manufacturers, limiting their ability to compete on cost in budget channels. This consolidation allowed brands like Motorola and Samsung to secure more share in prepaid outlets such as Cricket and Metro, but it also narrowed consumer choice. Apple, focused on higher-value devices and services, faced less competition from fringe players and benefited as the market shifted away from ultra-cheap phones. In effect, the weakness at the bottom of the market pushed more attention—and spending—toward premium platforms where Apple is strongest.

Apple Emerges as the Only Major Winner in Q1 2026

Taken together, these dynamics left Apple as the rare major vendor gaining smartphone market share Q1 2026 during a downturn. The company converted a strong iPhone 17 launch into sustained momentum by exploiting Samsung launch delays, maintaining attractive pricing on the iPhone 17e, and benefiting from a shakeout in the low-end segment. Counterpoint Research data shows that timing and product availability were at least as important as new features: Apple had inventory ready when buyers were in the market, while some competitors did not. As memory costs rise and economic pressures persist, the gap could widen if Apple continues to outspend rivals on promotions without hiking prices. For now, the iPhone 17 has not only weathered a difficult quarter—it has solidified Apple market dominance, leaving Android manufacturers scrambling to regain lost ground.