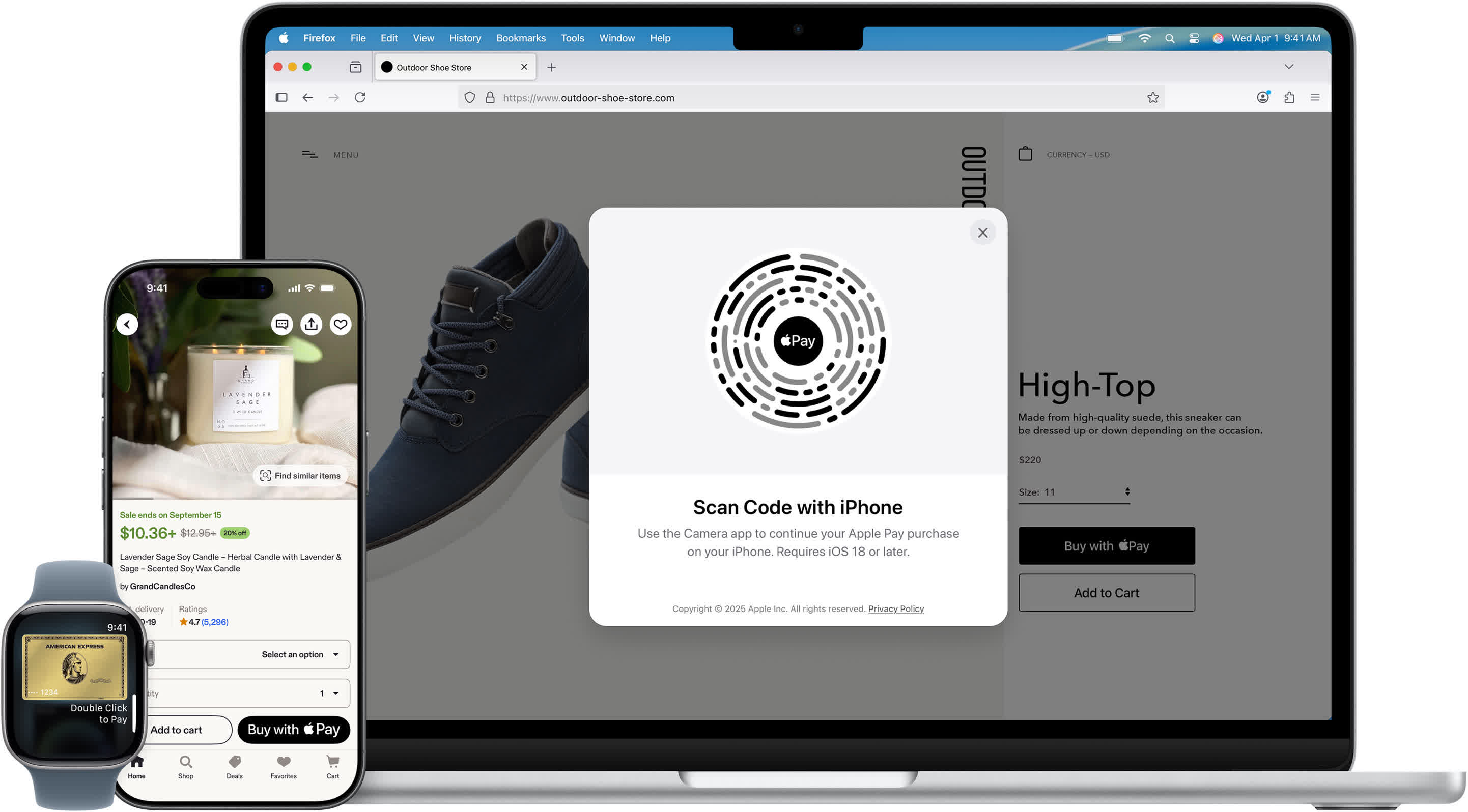

From Two-Second Tap to Complex Security Dance

On the surface, an Apple Pay purchase feels almost trivial: double-click the side button, authenticate with Face ID or Touch ID, tap your iPhone or Apple Watch, and wait for the beep. Behind that smooth interaction, however, is a dense stack of contactless payment technology working in lockstep. Near-field communication (NFC) provides the short-range wireless link between your device and the terminal, while EMV standards define how payment data is structured, verified, and authorised. In those brief seconds, your device, the merchant, the payment network, and your bank coordinate a secure conversation that never exposes your actual card number. Instead, Apple Pay security relies on payment tokenization, dynamic cryptograms, and digital wallet encryption bundled inside a dedicated hardware Secure Element. Understanding this hidden choreography helps explain why a quick tap can be both incredibly convenient and highly resistant to fraud and data breaches.

Tokenization and the Device Account Number: Your Card’s Stand-In

Apple Pay security starts when you add a card to Apple Wallet. Rather than storing your real card number, Apple Pay uses payment tokenization to create a Device Account Number (DAN) that is unique to that specific device. Your card details are sent to Apple only to identify the issuing bank and request a token. The bank then works with a Token Service Provider (TSP), which generates the token plus associated cryptographic keys and a CVV key. These are provisioned into the device’s Secure Element, analogous to a hardware security module, and tied to that one piece of hardware. From then on, all contactless payment technology flows through this DAN instead of your actual card details. Merchants only ever see the DAN and transaction-specific data, so even if their systems are compromised, attackers cannot retrieve your real card number from stored Apple Pay transactions.

Inside the Secure Element: Cryptograms, Dynamic CVV, and Encryption

When you authenticate with Face ID, Touch ID, or a PIN, Apple Pay unlocks the Secure Element just long enough to process a transaction. Inside this isolated chip live the DAN and cryptographic keys used for digital wallet encryption. For each purchase, the Secure Element generates a unique cryptogram by combining the token (DAN), token key, transaction amount, and payment token key. Simultaneously, it uses the CVV key provided at enrolment to produce a dynamic CVV that is valid only for that specific transaction. This bundle of data is encrypted and passed to the merchant application or terminal, never exposing underlying keys. Because every cryptogram and dynamic CVV is one-time use, replaying intercepted data will fail. This design turns your iPhone or Apple Watch into a tamper-resistant payment card that creates fresh, verifiable proof of each transaction without revealing sensitive long-term secrets to merchants or intermediaries.

How a Contactless Apple Pay Transaction Is Authorised in Seconds

Once the cryptogram and dynamic CVV are created, Apple Pay’s contactless payment technology hands control to the wider payments ecosystem. The merchant’s system sends the encrypted data to its Payment Service Provider (PSP), which decrypts it and forms a 3D Secure authorisation message. That message goes to the payment network (such as Visa or Mastercard), which recognises the DAN as a token rather than a primary card number. The network forwards the request to the Token Service Provider that originally issued the token. The TSP validates the cryptographic data, retrieves the underlying card details, and returns them to the payment network. The network then passes the real card information to the issuing bank, which verifies the dynamic CVV, checks available funds, and approves or declines the transaction. The approval flows back through the network, PSP, and terminal to your device—all typically completed in just a few seconds.

Why Understanding Apple Pay Security Builds Trust in Digital Payments

Apple Pay security is not magic; it is the disciplined application of tokenization, EMV standards, and strong cryptography. Your real card number is replaced with a device-specific token, sealed in a Secure Element, and used only within one-time cryptograms protected by digital wallet encryption. Merchants never see or store your actual card details, and every transaction carries its own dynamic CVV that banks can independently verify. Even if a payment terminal, PSP, or retailer suffers a breach, attackers gain only limited, unusable data rather than reusable card numbers. Compared with traditional magnetic stripe payments, this architecture drastically reduces the attack surface. Knowing how these layers work together—NFC as a transport, EMV as a protocol, and hardware-backed keys as the foundation—can help you feel more confident each time you double-click and tap, trusting that the two-second interaction is backed by a robust cryptographic system.