From Feature Creep to Fitness Tracker Fatigue

For more than a decade, wearables evolved by adding more sensors, bigger screens, and endless software tricks. Fitness trackers, smartwatches, and performance watches converged into devices that essentially did the same things, often more than most people actually needed. As a result, the market reached saturation: almost anyone who wanted a smartwatch already had one, and new models brought incremental tweaks rather than must-have upgrades. Hardware makers responded by pushing premium features down into cheaper tiers while nudging prices up and experimenting with subscriptions. But this model is running out of steam. Consumers increasingly see fitness tracking as a commodity rather than a luxury and are less willing to pay recurring fees for basic metrics. This fatigue with overbuilt devices and ongoing costs is the backdrop for the rise of budget smart bands and the mounting pressure on Whoop’s subscription-centric strategy.

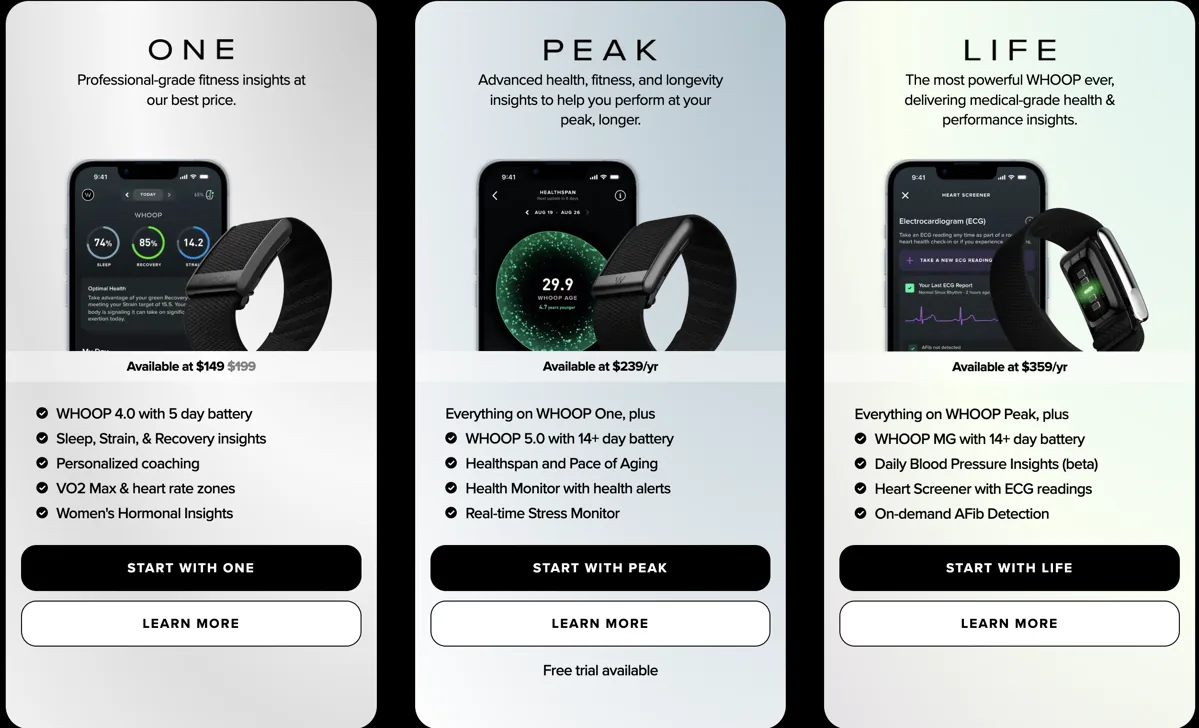

Whoop’s Subscription Fortress Meets a New Kind of Rival

Whoop carved out a niche by stripping hardware down to essentials—a heart rate sensor on a strap—and charging for the software that interprets the data. The device is effectively bundled with the subscription, and the app’s recovery scores, sleep guidance, and performance insights are what justify its annual fee of USD 239 (approx. RM1,120). For years, there were no true fitness tracker alternatives that matched this “smart band plus app” concept without a similar paywall. That allowed the Whoop subscription model to dominate serious athletes and data-obsessed users. However, the emergence of basic bands like Polar Loop, Amazfit Helio Strap, and Garmin’s Index sleep band signaled that other brands were willing to offer simple sensors that plug into existing apps. While early attempts felt either overpriced or underpowered, they opened the door for more affordable, more capable bands to attack Whoop’s core value proposition.

Fitbit Air Raises the Stakes for Budget Smart Bands

Google’s Fitbit Air is the clearest sign yet that budget smart bands are going mainstream. Priced at USD 99 (approx. RM465), it matches the Amazfit Helio Strap while leveraging Fitbit’s large user base and a mature app ecosystem. Crucially, its software aims to deliver analytics and coaching that feel similar in spirit to Whoop’s insights, but without requiring a recurring subscription fee. If the revamped app and its Health Coach features prove reliable, Fitbit Air will offer a compelling one-time purchase in place of Whoop’s ongoing cost. For non-elite users, “almost as good” data at a fraction of the annual outlay is likely good enough. This shift reframes expectations: instead of paying every year for core metrics like sleep, strain, and recovery, many consumers will expect those capabilities to be included in the purchase price of budget smart bands.

A New Monetization Playbook for the Wearable Market

As budget smart bands undercut premium subscriptions, wearable market competition is forcing brands to rethink how they make money. Hardware alone is no longer a reliable cash cow, yet users resist paying subscriptions for what they see as standard features. That tension is pushing companies toward hybrid models where basic tracking comes baked into low-cost devices, while advanced services sit behind optional paywalls. Whoop is already pivoting in this direction, repositioning itself less as a gadget maker and more as a health company. Through its app, users can now book blood tests and, newly, pay for video consults with healthcare professionals. Instead of monetizing every heartbeat, the company is betting on value-added services layered atop core tracking. If this approach succeeds, it could chart a path for other brands: sell affordable sensors, then upsell coaching, diagnostics, and personalized health insights.

What Consumers Will Expect from Fitness Tracker Alternatives Next

The rise of Fitbit Air and other budget smart bands signals a reset of consumer expectations. Core capabilities—continuous heart rate tracking, sleep analysis, and daily readiness metrics—are increasingly seen as table stakes, not premium perks. People want small, comfortable devices that disappear on the wrist yet deliver clear, actionable feedback in an app, all at accessible price points and with minimal ongoing costs. That doesn’t eliminate space for high-end offerings; dedicated athletes may still pay Whoop’s subscription to access niche metrics like detailed recovery from strength training. But the mass market is moving toward one-time purchases and simple, robust experiences. Over the next few product cycles, success in fitness tracker alternatives will likely hinge on who can offer the most value upfront while reserving truly differentiated features—like deep health integrations or expert coaching—as optional, clearly justified add-ons.