From AI Gold Rush to ROI Test

AI infrastructure capex is the large-scale capital spending on cloud data centers, accelerators and networking that powers modern AI workloads, and it is increasingly judged on whether the resulting AI services generate durable revenue growth, strong margins and measurable customer value rather than short-lived hype or capacity alone. After two years of AI enthusiasm, earnings season shows the market shifting from narrative to economics. Valuations are being reset, and software names that once benefited from an automatic “AI premium” now must prove that enterprise AI spending translates into cash flows. The gap between promised AI demand and the cost of building data center capacity is at the center of this reassessment. Winners are those that can tie AI directly to mission‑critical workflows and recurring revenue; laggards are seeing their multiples compress even when headline growth looks solid.

Oracle’s $50 Billion Bet and the Data Center Economics Question

Oracle’s upcoming Q4 FY2026 earnings are a live test of data center economics in the AI era. The company has signaled FY2026 revenue of USD 67 billion (approx. RM308.2 billion) alongside capital expenditures of USD 50 billion (approx. RM230 billion), a level of AI infrastructure capex that forces investors to examine cloud computing ROI rather than top-line growth alone. Its remaining performance obligations reached USD 553 billion (approx. RM2,543.8 billion) at the end of Q3 FY2026, strengthening the case for Oracle Cloud Infrastructure as an AI platform while highlighting the capital intensity required to deliver that backlog. Mizuho analyst Siti Panigrahi expects solid revenue and earnings, but the harder question is whether borrowing to fund server capacity can stay below USD 100 billion (approx. RM460 billion) and still produce acceptable returns as enterprise AI spending matures.

CrowdStrike and Rubrik: AI Infrastructure with Execution Risk

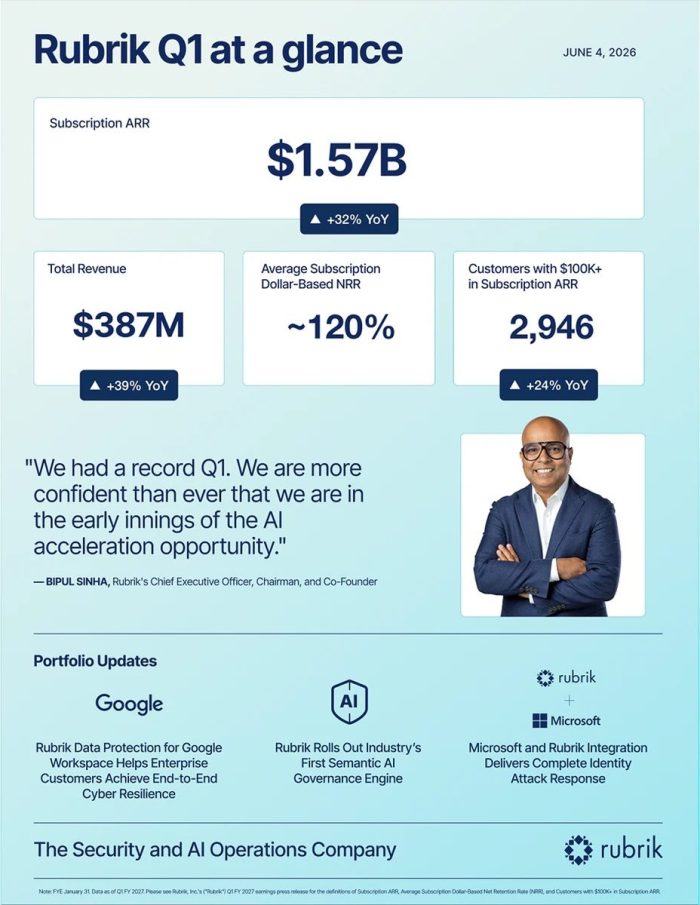

Security and data infrastructure vendors show both the opportunity and the pressure around AI-linked valuations. CrowdStrike’s latest quarter featured revenue of USD 1.39 billion (approx. RM6.39 billion), up 26% year over year, with annual recurring revenue reaching USD 5.51 billion (approx. RM25.34 billion) and free cash flow of USD 468.5 million (approx. RM2.15 billion). Management tied AI directly to the Falcon platform, agentic tools and projects such as Mythos, Project QuiltWorks, AIDR and Charlotte AI, positioning cybersecurity as a practical outlet for enterprise AI spending. Yet the after‑hours reaction underlined how unforgiving investors have become toward stocks with an AI premium. Rubrik, meanwhile, reported 39% revenue growth to USD 387.1 million (approx. RM1.78 billion) and subscription ARR up 32% to USD 1.57 billion (approx. RM7.22 billion), displaying how AI‑driven data protection and cyber resilience can turn into high‑margin recurring revenue.

Software Valuations Split: Intuit’s Slump and AI-Ready Platforms

The software sector is where the divide between AI-ready infrastructure vendors and threatened incumbents is most visible. Intuit’s share price has fallen about 50% year to date and more than 55% over the past 12 months, despite third‑fiscal‑quarter revenue of USD 8.6 billion (approx. RM39.56 billion) growing 10% and earnings per share beating estimates in each of the last four quarters. According to Forbes, Intuit has become the worst performing stock in the S&P 500 so far this year, even as management raises earnings guidance and expands buybacks and dividends. Analysts at Goldman Sachs and Bank of America worry that generative AI tax tools could erode TurboTax’s moat. Across SaaS, forward price-to-earnings ratios have dropped from about 35 times to 20 times, showing that investors no longer reward AI stories without clear data center economics and cloud computing ROI.

Enterprise Buyers Want Proof, Not Promises

For enterprise technology leaders, the message from these earnings is clear: AI infrastructure investments must prove their worth in business terms. Buyers are tightening criteria for AI infrastructure capex, asking how much each dollar spent on GPUs, storage and networking contributes to revenue, cost savings or risk reduction. Vendors like Oracle, CrowdStrike and Rubrik are responding by tying AI directly to workflows in ERP, security operations and data resilience, and by pointing to metrics such as ARR growth, cash flow and contribution margins. At the same time, the drawdown in software valuations shows that markets will penalize platforms seen as exposed to AI commoditization. The next phase of enterprise AI spending will favor providers that can balance rapid capacity expansion with disciplined data center economics, transparent pricing and referenceable customer outcomes, rather than those selling undifferentiated AI capacity.