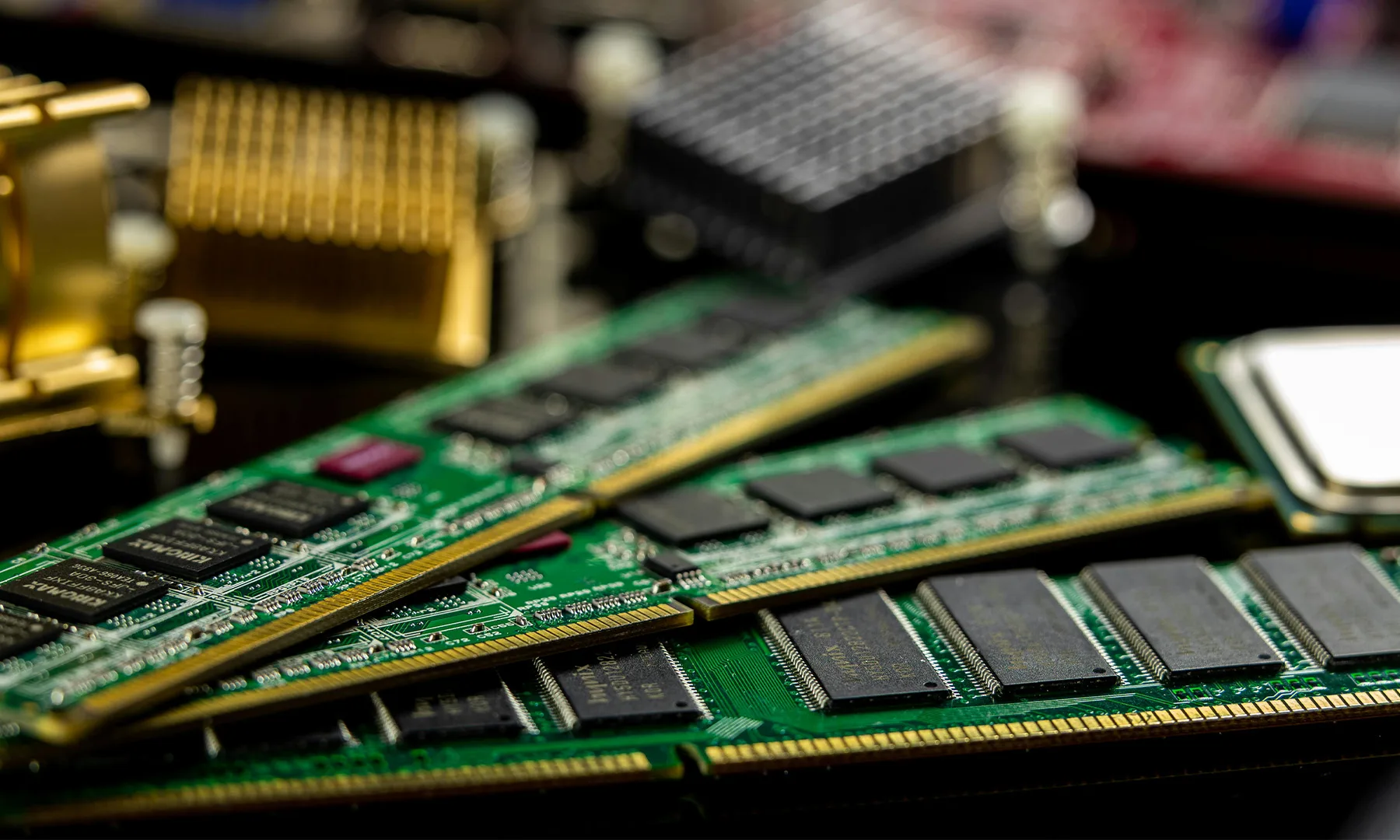

How the AI Boom Broke the Memory Market

Over the past year, PC builders have faced a brutal spike in memory costs as AI infrastructure devoured the global supply of DRAM and NAND. Major manufacturers such as Samsung, SK Hynix, and Micron redirected capacity toward lucrative high-bandwidth memory (HBM) for AI accelerators, leaving far fewer wafers for mainstream RAM and SSD components. Fixed DRAM transaction prices jumped 20–50% month-on-month from April 2025, while NAND flash climbed 4–11% in the same period. For consumers, that translated into midrange DDR5 kits that once cost around USD 200 (approx. RM920) now selling closer to USD 350 (approx. RM1,610), with similarly painful SSD increases. This AI-driven “memory supercycle” created a supply squeeze that pushed PC builder costs to unsustainable levels and left desktop and laptop buyers effectively subsidising data-centre AI deployments.

Chinese DRAM and NAND Capacity Changes the Equation

A new wave of production from Chinese memory makers is starting to challenge that imbalance. Yangtze Memory Technologies is reportedly consuming around 500,000 domestically produced wafers each month for 3D NAND, signalling substantial flash capacity aimed squarely at SSDs and data storage. On the DRAM side, ChangXin Memory Technologies (CXMT) has quietly grown to nearly 8% of the global DRAM market and is aggressively ramping DDR5 output, with speeds up to 8000 MT/s already on its roadmap. In parallel, other vendors are scaling data-center memory products, creating a broader ecosystem instead of a single niche player. Because memory pricing is highly sensitive to even modest shifts in supply, this influx of lower-cost DRAM and NAND gives buyers alternatives to the dominant trio and is the first real structural pressure against AI-fuelled price escalation.

Corsair’s Move Puts Chinese RAM in the Mainstream Spotlight

The clearest sign that this shift is real is the arrival of Chinese DRAM inside well-known consumer brands. Leaked module readouts show Corsair’s Vengeance DDR5-6000 kits using CXMT chips, with specifications such as 6000 MT/s and CL36 timings that align with comparable modules based on Samsung and SK Hynix dies. Market reports suggest some CXMT DDR5 modules are being sold near the USD 150 (approx. RM690) range, while similar products from traditional suppliers can hover between USD 300 and USD 400 (approx. RM1,380–RM1,840). That kind of price spread immediately gives major PC component makers bargaining power, even if they do not fully switch suppliers. Still, one successful kit does not equal parity: system builders will be closely watching long-term stability, firmware behaviour, and compatibility before rolling Chinese memory out across entire product lines.

When Real RAM and SSD Price Relief Is Likely

Despite visible progress, price relief will not be instant. Kye-hyun Kyung, former head of Samsung’s chip and display division, predicts that meaningful DRAM price drops are more likely in the second half of next year, assuming Chinese investments mature and translate into sustained high-volume output. In the near term, AI demand for HBM remains intense, and any incremental supply may first stabilise prices rather than slash them. Oversupply warnings from analysts suggest the balance could eventually tip, especially if Chinese fabs continue scaling aggressively while data-centre spending normalises. For PC builders, that means RAM price relief and an SSD price decrease are plausible over the next 12–18 months, but not a return to the rock-bottom levels seen before the AI boom. Instead, expect a gradual correction that narrows the gap between enthusiast ambitions and real-world budgets.

Long-Term Impact on Hardware Pricing and Competition

Beyond short-term DRAM price drops, the rise of Chinese memory makers hints at a deeper realignment of hardware economics. If CXMT, Yangtze Memory Technologies, and peers can prove reliability at scale, they will become permanent alternatives rather than temporary bargaining chips. That competition could reshape contract negotiations, encourage more diversified sourcing, and reduce the risk that any single technology trend—like AI HBM demand—can distort the entire market. However, there are still headwinds: questions around yield, quality consistency, and long-term support must be answered, and geopolitical tensions over chip technology could disrupt supply chains just as they mature. Even so, this is the first credible challenge to the entrenched pricing power of the current leaders in years, and it offers PC builders a realistic path to more predictable RAM and SSD costs over the long run.